You don’t need to comb the pages of the Wall Street Journal or the Financial Times to know what’s going on with the economy. Just take a look at Bloomberg Bonds and skip-down to the price/yield section on 10-year US Treasuries. That will tell you everything you need to know.

As of Monday, yields are at 1.66%, a little higher than they have been lately, but still ridiculously low in what many people are calling the 4th year of the recovery.

Recovery? You’ve got to be kidding. 1.66% is below the rate of inflation, which means that if you plunk your money into a 10-year bond, you’ll get back less than you put in. (inflation adjusted) Great investment, eh?

So, why are rates so low?

First of all, because people are still scared because the government and the Fed haven’t fixed anything and keep implementing strategies that people don’t understand.

Second, because there’s no competition for money, no demand for new loans, because homeowners and consumers are still licking their wounds from the meltdown and need to get their balance sheets together.

Third, because big business has nothing to invest in except the goofy structured finance products that went toes-up when the sh** hit the fan in 2008. (CDO’s anyone?)

Forth, Europe. The big money is still exiting the sinking continent to safe haven Treasuries. (USTs are still the cleanest shirt in the hamper.)

And, fifth, rates are low because we’re ruled by idiots. How else would you explain the fact that the Fed has initiated 3 rounds of bond buying (QE) to the tune of many trillions of dollars and unemployment is still above 8 percent, underemployment is above 15%, 13 million people still can’t find jobs, consumer confidence is down, retail sales are flagging, the housing market is in the dumps, domestic manufacturing is contracting, business investment is anemic, and credit expansion is zilch excluding rip-off student loans and junk subprime auto loans?

How is it that Mr Bernanke–who never saw the housing bubble, who sang the praises of knucklehead mortgage products that blew up the financial system, and who assured us that the housing implosion was “contained”– can keep his job as chief regulator and monetary policymaker with this abyssmal record of failure?

The economy cannot possibly improve as long as the man in the wheelhouse is a dunce. That much is certain. Rates are low mainly because of the criminal mismagement of the economy.

Did you know that people are stuffing boatloads of money into their mattresses to avoid investing in the transparently rigged stock market? It’s true. Here’s the scoop from TrimTabs:

“TrimTabs Investment Research said today that inflows into checking and savings accounts are far outpacing inflows into all other major investment vehicles….

In a research note, TrimTabs explained that checking and savings accounts attracted a combined $356 billion in the first half of 2012, nearly double the inflow of $188 billion into bond mutual funds and exchange-traded funds….

“Inflows into savings accounts were consistently heavy—the flows weren’t just happening in one or two months,” noted Biderman. “Savings account inflows ranged from $30 billion to $90 billion in each of the first six months of this year.”

Now if you or I, dear reader, were assigned the task of restoring faith in the capital markets, and yet, 4 years after the Lehman debacle, people were still squirreling their money away in regular zilch-interest “vanilla” bank accounts, we’d get our “walking papers”, right? But not easy-money Bennie, the Pride of Princeton. Oh no. Bernanke gets a pat on the back and another 6 years to drive the world’s biggest economy deeper into the ditch. Go figure?

Of course, the state of the economy doesn’t matter to Bernanke as long as the “people who count” are still making money. Take a look at this:

“The only major metric I looked at wherein today’s recovery outperformed the average expansion of the previous 60 years was corporate profits. In the average postwar recovery, corporate profits rose 38 percent from trough to peak. So far into this recovery, they have risen 45 percent.”

So big business is raking in the gravy while everyone else has been scraping by trying to put food on the table or stay out of the poor house. Are you surprised?

In the same article, Rampell notes that government spending has actually seen “smaller growth in this recovery than in any previous ones …. In fact, the public sector has not grown at all in the last three years; it is smaller today than it was when the recovery began.”

How about that? So all that baloney about Obama being a “big spender” is just more GOP propaganda. There’s not a word of truth to it. The administration should have boosted the size of the American Recovery and Reinvestment Act (ARRA), as every competent economist in the country had warned. Instead, Obama went with the recommendations of Wall Street favorite, Larry Summers, who torpedoed Christina Romer’s appeal for a $1.8 trillion stimulus and set the stage for today’s protracted slump. Interestingly, there was an article in the Washington Post just last week that confirmed once again that –according to the data–the ARRA did just what it was supposed to do. The only problem was that it was too small. Here’s a clip from the article that drives home the point:

“At its peak, the Recovery Act directly employed more than 700,000 Americans on construction projects, research grants and other contracts. That number doesn’t include the jobs saved or created through its unemployment benefits, food stamps and other aid to struggling families likely to spend it; its fiscal relief for cash-strapped state governments; or its tax cuts for more than 95 percent of workers. Top economic forecasters estimate that the stimulus produced about 2.5 million jobs and added between 2.1 percent and 3.8 percent to our gross domestic product….

It’s true that a bigger stimulus would have provided a bigger economic jolt and accelerated the sluggish recovery. More public works projects would have produced more jobs; more state aid would have prevented more of the public-sector cutbacks that have slowed the recovery; more tax cuts would have directed more cash into your wallet.”

That settles it, stimulus works. Fiscal stimulus, that is. Monetary stimulus, on the other hand, is a total dud, unless, off course, the goal is too pump more helium into hyper-inflated equities to keep the investor class cheery. If there’s any doubt that that was Bernanke’s real intention, then take a look at this chart of QE’s performance over the last few years. The chart shows how stocks rose on an ocean of Fed-generated liquidity while the economy stagnated and the jobless numbers barely budged.

Diminishing returns on bond buying make it less likely that Bernanke will initiate another round of QE, mainly because the Fed’s accommodative policy (The “Bernanke Put”) hasn’t increased the amount of money in circulation, which means that QE is having negligible effect on the real economy. The so-called transmission mechanism is on the fritz, leaving the Fed without the tools it needs to kick-start the economy. British economist John Maynard Keynes warned that monetary policy alone would not be sufficient to trigger economic recovery during a massive deleveraging cycle like today, but Bernanke doesn’t like Keynes, so we can probably expect more of the same. QE to infinity.

There are a number of ways to measure Bernanke’s dreadful effect on the economy, the most obvious of which is GDP. How much is the economy actually growing, that’s the question?

Not much, it appears. Take a look at this:

“According to the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters, real gross domestic product is expected to grow at only a 1.6% annual rate this quarter and 2.2% in the fourth quarter, down from 2.5% and 2.6% forecast three months ago…

Lower economic activity forecasts are leading to reduced expectations for job growth. The forecasters now see payroll gains averaging 125,000 per month this quarter and 135,300 in the fourth. That hiring pace is down sharply from the gains of 170,000 and 172,600 expected in the second-quarter survey.

Slower hiring means the U.S. unemployment rate will remain above 8% until the second quarter of 2013. In the previous forecasts, the economists thought the rate would fall below 8% by the fourth quarter of this year.” (“Economists in Philly Fed Survey Lower Forecasts”, Wall Street Journal)

Be real. The truth is, the economy is probably already in recession, but the data won’t show it for another quarter or so. But consider what this information on GDP means in terms of what we have already gone over in this article. First, that monetary stimulus (quantitative easing) hasn’t worked for 4 years. Second, that fiscal stimulus did work. That said, which type of stimulus do you think the administration should pursue?

It’s a no-brainer, right?

One last thing about interest rates: Sure, Bernanke’s low rates make it easier for people to pay their bills, (because it reduces the real burden of debt) or for banks to finance their stinkpile of garbage loans. It also makes it cheaper to buy a house or car or whatever. This is the upside of cheap money. But there’s a downside, too. Many people are putting off retirement because they can’t make the money on their savings and investments that they figured they’d be able to. The Fed’s policy is forcing them to hang onto the jobs longer than they would have in a normal rate environment. That’s having a very damaging effect on younger people entering the workforce who can’t land a job because Gramps is still manning the key-puncher. Here’s how Dr. Housing Bubble sums it up:

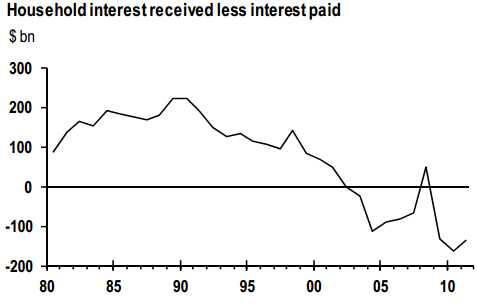

“Net US household interest income is pushing record lows,” which means that the perennial low rates are “pushing costs in other areas of the economy.” Just check out this chart and you’ll see what’s going on.

Bernanke is essentially ripping off retirees and savers to provide the banks with cheap capital. At the same time, he’s putting the kibosh on young graduates and others from getting the job they need to start their careers or enter the middle class. This is the downside of the Fed’s misguided low rate regime.

Low rates mean that the economy is going to be in a funk for a very long time unless the policy changes.

That’s why Mr. Bernanke needs to get his pink slip pronto.

MIKE WHITNEY lives in Washington state. He is a contributor to Hopeless: Barack Obama and the Politics of Illusion. He can be reached at fergiewhitney@msn.com

{kind=link}