Thus far, the highly controversial corporate bond buying programs that the Federal Reserve first announced on March 23 have yet to spend a dime according to a spokesperson for the New York Fed, the regional Fed bank that is overseeing almost all of Wall Street’s emergency bailout programs today as well as during the financial crash of 2007 to 2010.

But as the above chart indicates, just a promise from the Fed to spend billions removing toxic waste from Wall Street’s mega banks is enough to put a bid back in the junk bond market.

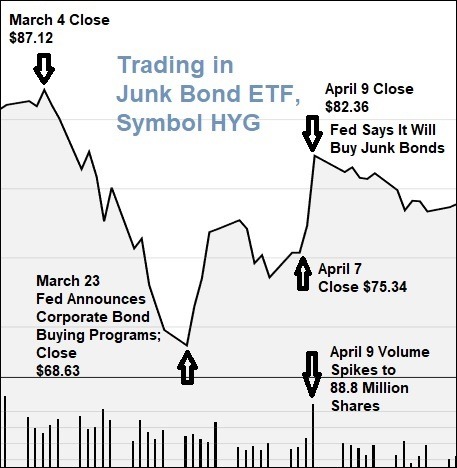

Here’s the skinny on how the Fed propped up both the Dow and the junk bond market with its well-timed announcements on March 23 and April 9.

From the close on March 4 to the close on March 23, the junk bond exchange traded fund (ETF) which goes by the fancy title of “iShares iBoxx High Yield Corporate Bond ETF,” or symbol HYG, lost 21 percent of its value. But that weakness in the junk bond market did even worse damage to the Dow Jones Industrial Average. Over those same trading days, the Dow lost 8,498.93 points or a stunning 31 percent of its value in just 14 trading sessions. (See chart below.) That had apocalyptic overtones for what lie ahead for the balance of the year.

There are two key reasons for the correlations between the junk bond market and the Dow. The first is that two of the Wall Street banks that were a regular presence in the Wall Street syndicate that underwrote these junk bond offerings are components of the Dow’s 30 stocks. Those two banks are Goldman Sachs and JPMorgan Chase. The second key reason is that if Goldman Sachs and JPMorgan Chase are tanking, they will inevitably bring down the share price of every other major Wall Street bank because of their heavy interconnections as derivative counterparties to each other. (If all of those banks enter a serious selloff, the Fed could be looking at another 2008 financial crash after assuring Americans for years that these banks are “well capitalized.”)

In short, thanks to the repeal of the Glass-Steagall Act in 1999, which allowed Wall Street casinos to merge with the largest federally-insured, deposit-taking banks in the country, we now have a central bank (the Fed) that believes its job is to throw money at any market that pulls down the Dow. Because damage to the Dow might damage consumer confidence which might damage the wealth effect which might damage consumer spending which might damage the next GDP report which might damage the vision of American exceptionalism. In other words, we’re all just Labradoodles now in fealty to Wall Street.

Two simple solutions to the Fed’s conundrum would be to restore the Glass-Steagall Act and restore corporate pension plans which offer a guaranteed (defined benefit) at retirement, thus cutting the cord between consumer spending/consumer confidence and the health of the worker’s 401(K) plan as measured by the health of the Dow Jones Industrial Average. (See our 2008 article, Wall Street’s Collapse and the Ownership Society.)

The Fed’s balance sheet as of last Wednesday had ballooned to $6.6 trillion as it throws money in all directions to snuff out fires on Wall Street. If you add that to the federal government’s outstanding debt of $24.7 trillion, that’s $31.3 trillion of debt that we’re leaving as our legacy to the next generation.

To show just how pressured the Fed is to prop up any market that tanks, let’s look at the timeline that goes with the chart above. On March 23, the Fed announced that it was creating two facilities to buy up investment grade corporate bonds along with other programs. The corporate bond facilities were called the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF). In that announcement, the Fed said that the two facilities would only be buying investment grade bonds. That was good enough news for the HYG ETF which rallied through March 30.

But then HYG’s share price began to sag again along with the rest of the junk bond market. So on April 9, in a long-winded press release purporting to be taking actions to help everyday Americans, the Fed changed its Terms Sheets for both the PMCCF and the SMCCF and announced that the Fed, for the first time in its 107 year history, would be buying junk bonds. The caveat was that the bonds would have had to have been rated investment grade as of March 22. (In reality, a large swath of the lower-rated investment grade bonds were going to be downgraded to junk even if the coronavirus COVID-19 outbreak had not occurred.) And, just as the junk bond ETF market had figured correctly all along, the Fed in its updated April 9 Term Sheet for the SMCCF announced that it would also be buying junk bond (a/k/a high yield) ETFs.

That April 9 announcement came at 8:30 a.m., one hour before the stock market opened. The shares of HYG rallied strongly on volume of 88.8 million shares, more than twice the volume of earlier in the week.

In recent days the rally in HYG and the junk bond market in general is beginning to fade. It will be interesting to see what hat trick the Fed attempts next.

This story first ran on Wall Street on Parade.