Finance, Wall Street and the increasingly intrusive economy that by design is taking over ever-larger portions of the public space, should by rights have gone into decades-long hiding around 2007. As much as ‘bottom-up’ explanations of greed-crazed citizens driving bankers to behave in ways they shouldn’t fill the bourgeois imagination, bankers and their servants in ‘public’ office have driven the current epoch of finance capitalism since it was launched in the late 1970s. Through official channels the tale is of sin and redemption, crisis followed by righteous and robust recovery. Sure a few (tens of millions) people may have ‘lost’ their jobs, houses and life savings, but such are the dynamics of political economy that rewards talent and hard work.

For those who only have occasional time / interest to follow the political and economic debate, the latter is the ‘left’— Democrat, liberal and progressive, explanation of the last few decades followed by a plea that we do more to help ‘the unfortunate.’ Fortune in this incarnation harkens to Machiavelli’s fortuna as the caprice of the universe against which prudence is the partial and only mitigation. Ironically, prudence is the opposite of ‘dynamic’ capitalism, the reckless abandon with which those with less to lose than the rest of us live as heroes in their own, and occasionally the social, imagination. Aiding this dance are the explainers— bourgeois economists and liberal politicians, whose public roles depend on plausibly selling the intersection of calculation and caprice no matter how inconvenient the ‘facts.’

Graph (1) above: in contrast to the ‘greedy borrower’ explanation of the financial and economic decline that started around 2007, bankers spent the prior decades lobbying politicians to reduce restrictions on the types and amounts of mortgage loans they could make. Illustrated above is the relation of mortgage lending to house prices measured as rates of change. While cause and effect are often difficult to determine, the quantity and rate of growth in mortgage lending rapidly rose after restrictions on bank lending were removed. Through this process bankers drove mortgage lending, and with it house prices, higher in the boom and lower in the bust. The growing disconnect between house prices and mortgage loans since 2009 reflects hedge funds buying houses wholesale to rent back to dispossessed home ‘owners’ using cheap money created by the Federal Reserve. Source: St. Louis Federal Reserve.

In contrast to general perceptions and the economic mythology of the radical ‘center,’ the major hindrance to economic, and with it political, reconciliation in the present is the faux-Keynesian explanation of banking and money that places bankers as allocators of savings and limits credit creation through fractional-reserve banking. In practical terms, given that bankers were free to create the housing boom and bust, what is the limit on their capacity to drive other economic outcomes? And the housing boom and bust in the U.S. is but one aspect of global (‘private’) credit-driven economy that separates ‘winners’ from ‘losers’ through digital entries to bank accounts and private security forces.

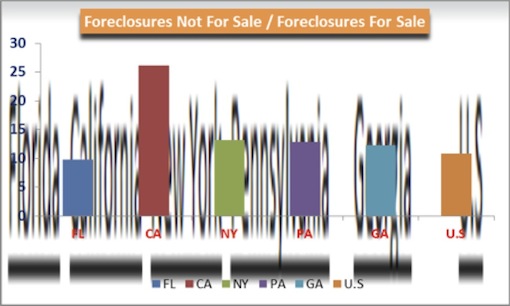

At ground level many readers may be surprised to learn that in California in 2015 there are twenty-six foreclosed or soon to be foreclosed houses that aren’t for sale for every foreclosed house currently for sale (source: Zillow). Nationally, the ratio is about 10:1 foreclosures not for sale to every foreclosed home that is for sale. The problem isn’t simply that bankers created a temporary economic downturn in 2007 that government was forced to address through bailouts. Eight years later poor and formerly middle-class neighborhoods in large and mid-sized cities across the U.S. are being turned into zombie housing ghettos where housing won’t ‘recover’ for their citizens in their lifetimes. This is both fact and metaphor for the zombie countries and regions being created by Wall Street and its economic replicants around the world.

Graph (2) above: This graph scales the number of current and soon-to-be foreclosed houses to those for sale. For instance, Florida has about ten foreclosed and soon-to-be-foreclosed houses for every one foreclosed house that is for sale. California has about twenty-six foreclosed and soon-to-be-foreclosed houses for every foreclosed house that is for sale. Nationally, there are about eleven foreclosed and soon-to-be-foreclosed houses for every foreclosed house that is for sale. Putting this ‘shadow inventory’ of foreclosed houses up for sale would increase the number of houses for sale nationally by about thirty percent. Given the concentration of the housing bubble and bust on the two coasts and in major cities, adding this shadow inventory would instantly crash the national housing market. Source: Zillow.com.

These issues are no doubt abstract, but understanding the economics is essential to resolving the current predicament of the global economy. In the late 1990s and early-mid 2000s bankers were able to drive house prices higher, to create a housing ‘bubble,’ through increasing the quantity of mortgage credit available— the bubble was credit supply driven with credit demand following supply. Central Banks provide unlimited reserves to banks at a benchmark rate meaning that the money ‘multiplier’ is irrelevant to the quantity of loans that banks can make. Reducing lending standards, as mortgage bankers did in the housing bubble, relates price to quantity through ‘quality’— loan prices fell as riskier (more predatory) loans were made— the opposite of what is claimed by mainstream models that relate credit supply to demand through price. As Central Bankers have been explaining for some years now, the bourgeois economist’s frame is nonsense.

The practical impact is that liberal academics argue that the housing bust destroyed wealth without explaining the genesis of the bubble that led to it in monetary policies that they support. The Federal Funds rate set by the Federal Reserve is the price of bank reserves. Because the Federal Funds rate is considered a base rate, it serves as a proxy for other short term rates. Liberal and progressive economists argue that lowering or keeping this rate low boosts the economy by lowering business and consumer borrowing costs while falsely claiming that bank credit is limited by bank reserve ratios that are in fact fluid. The term multiple equilibria, as in many supply and demand relations, applies a rational patina to this process that history (think Great Depression) doesn’t support.

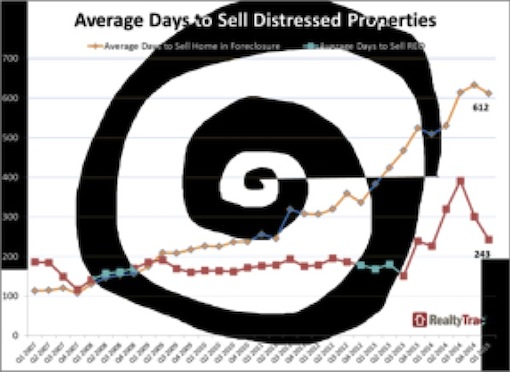

Graph (3) above: Those with an interest might ask themselves why, eight years and $11 trillion in global QE (Quantitative Easing) later, it takes on average two years to sell foreclosed houses? The foreclosure process should be cumbersome to protect the millions of people defrauded by banks. But as Graph (2) (two up) illustrates, the proportion of already foreclosed houses being held ‘off-the-market’ is far greater than that being offered for sale. Combine this with it taking two years to sell foreclosed properties once they are brought to market (Graph (3) above) and bankers know that they would quickly end the ‘housing-market-has-recovered’ storyline if these houses were offered for sale. Source: Realtytrac.

There is undoubtedly more to financial bubbles than undisciplined and / or lemon-socialist bank lending. But a relevant question is how it is that changes in bank credit drove house prices higher then lower (Graph (1) above) is reconciled with the mainstream argument that monetary policies were / are ‘neutral’ with respect to prices? The question gains tangential relevance as ‘private’ credit growth in China drove seven years of rapid economic expansion culminating, for the moment, in the financial and economic implosion that appears to be under way. Eight years after onset of a housing bubble in the U.S. neighborhoods across the country are being turned into housing-induced wastelands. Expand the problem and we get current circumstances in the European periphery and now apparently in China.

Economist Paul Krugman went so far as to list the Podunk crony-capitalist schemes employed by the Chinese government to stem the fall of Chinese stocks apparently not realizing that this exact same list, with the possible exception of chanting, describes U.S. policies to stem the fall of U.S. stocks in 2008. And in fact, it is this same insistence that bank money, 95% + of money created in the U.S., doesn’t matter; only its price does (the zero lower bound), that unites liberal and progressive policies with Wall Street’s interests. The visible ‘recovery’ in the U.S. economy has centered on asset prices— financial markets and housing. Anyone with an interest can go house by house to see the American economic periphery where half or more of the houses for sale (auction actually) were last occupied years ago when they were bought for $200,000 – $700,000 and are now ‘selling’ for pennies on the dollar but are so run down that they will never sell.

Picture (1) above: Housing is a ‘wasting’ asset, to the extent that one accepts the financialized frame for basic human shelter, because it substantially deteriorates without constant upkeep. Houses that are left to decay through drawn out social negotiations tend to require far more resources to be made livable again than to maintain. Additionally, once houses have been ‘financialized’ they are subject to capitalist arithmetic that seeks to maximize economic extraction no matter the social costs. Engineered economic crisis and the engineered aftermath have created a Tale of Two Cities in neighborhoods and cities around the world with connected insiders like hedge funds receiving free billions to buy whole neighborhoods in bulk and petite-capitalists playing landlord house by house. Original image source: amerifirst.com.

A few center-left economists correctly predicted that the housing bubble would end badly. The predictions / analyses tended to be based on relationships like house prices to incomes, rents and the broader economy (GDP)— they weren’t ‘causal’ in relating bank credit creation (Graph (1) above), or any other factor, to the improbable rise in house prices. And the first order remedies like aggressive fiscal policies to offset the resulting economic calamity might have ‘worked’ had they been so designed and implemented. But they weren’t. As the facts have it, were persistently low interest rates ‘good’ for the poor and middle classes thirty five years of declining interest rates would seemingly have ended poverty and unemployment. Unless one only ‘counts’ the time between crises, the U.S. is now fifteen years into economic decline in fits and starts.

The term ‘sado-monetarists’ was coined (apologies) to describe restrictive monetary policies in an economic downturn. But unless the cause of the downturn is ascribed to ‘nature,’ particular social choices led to it. The growth in bank credit in the late 1990s and early-mid 2000s led to a thin economic boom followed by a broad and pronounced bust. The ‘benefit’ of the boom wasn’t symmetrically distributed and neither were the costs of the bust. Following, a renewed boom for Wall Street and various and sundry financial interests has led to another thinly distributed economic ‘benefit,’ significantly to those who benefited from the last boom. With the last bust still being felt by those who saw little to no benefit from either boom, the argument that more of the same in the form of expansionary monetary policies will do the trick certainly requires straightforward explanation.

Another way to see the problem is that there is no necessary reason why the ongoing foreclosure crisis should be left to the banks that created it. Social resolution would be for the government to hire the unemployed at living wages with benefits to fix the lower-end housing stock and use it as low-cost public housing possibly giving it outright, or through an income based rent-to-purchase program, to the poor and dispossessed and charge the difference, if there is any, to the banks. The point isn’t to suggest better public policies that stand no chance of being implemented, but rather to contrast the possibilities against the path chosen to make the point that liberals and progressives in academia and public office are talking out of their rears in suggesting that monetary policies that only benefit the wealthy are better than nothing.

A quick guess given emerging circumstances in the global economy is that we are weeks, months, or at best a year or two from renewed crisis that will bring to the fore the folly— and class interests that have been served, by the public policies put into practice since crisis began in 2007. The interest here isn’t in improving public policies to ‘reform’ the current system of political economy. It is to gain and effectively communicate clear understanding of the social-economic mechanics of this epoch. What is clear is that economic paths have diverged in the last forty years and continue to do so. The eternal view from the center-left is that history has ended, that sequential crises of increasing intensity are accidents following which repairs must be made. Meanwhile, the trajectory for increasing numbers of people is persistent diminishment of circumstance.

Finally, to the economic ‘optimists,’ turn off the television and look around. What is apparent is that there are multiple ‘economies.’ And the one most of us depend is far from ‘recovered.’ What has ‘recovered’ is what was made to recover. Economic problems are still unfolding— current trajectory has parts of cities and whole towns turning into ruined housing wastelands. In this sense Detroit, parts of Chicago, St. Louis, Cleveland, Philadelphia, Baltimore and other large and mid-sized cities are the future for a lot more of the developed West. This dissolution is race and class based by design from ‘above.’ Racist and classist economic policies are racist and classist even if the intent is economic gain rather than more straightforward social repression. Unless history has ended, the future starts now.

{kind=link}