In his book Globalization and Its Discontents former World Bank economist Joseph Stiglitz details the ignominious history of IMF ‘structural adjustment’ programs inflicted around the globe in the 1990s. While the IMF has admitted that economic austerity is both theoretically flawed and socially destructive it remains a core IMF policy and is currently being forced on peripheral Europe. This institutional persistence is characterized by the Western economic mainstream as an accident of history, as flawed theories driving bad policy decisions. Another explanation that also fits the facts is that the IMF is a tool of Western economic power used to extract wealth from poor countries under the contrived apologetics of the ‘market’ economics it claims as its goal.

The point of interest here is the difference in interpretation— policies based on flawed theories or class interests expressed through nominally ‘neutral’ international institutions. These are joined together in Italian theorist Antonio Gramsci’s notion of hegemony as embedded premises and beliefs that support a given social order. This idea in some measure renders intentions irrelevant— the facts of institutional persistence are what they are. Actual social resolution comes through changing the balance of political and economic power. Institutions like the IMF and the Federal Reserve exist to support and maintain the existing order. Otherwise, why have ‘rational’ policy debates done so little to redirect demonstrably disastrous policies?

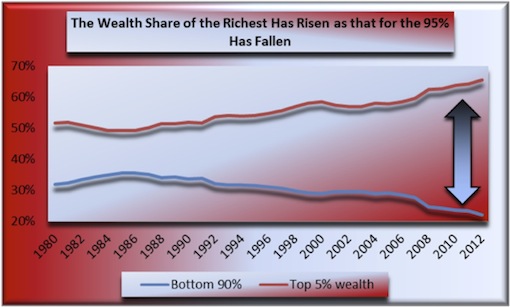

Graph (1) above: growing income and wealth ‘inequality’ in capitalist economies is well-covered territory. But the contention that capitalism is directly responsible for it is paradoxical. On the one hand inequality defined as differentiated economic outcomes is the point of capitalism. On the other, state capture— ‘public’ policies that always and everywhere benefit the existing social order, better explain the growing concentration of wealth than do ‘market’ theories of economic distribution. The graph illustrates the trend since the 1980s of the growing concentration of wealth at the very top. The trend increased dramatically since 2009 when ‘monetary’ economic policies like QE (Quantitative Easing) were implemented. Source: Emmanuel Saez.

The oft repeated saw that Western economics deals only with solved social problems promotes the premise that the problems under consideration were ever actually solved. By 2008 it was apparent to all who have eyes that the current epic of finance capitalism wasn’t / isn‘t working for most people. Since then the recovered confluence of financial and social power, with substantial support from quasi-public institutions like the Federal Reserve, has led to increasingly concentrated and potentially destabilizing economic mal-distribution. Policy ‘debates’ like expansionary austerity versus Keynesian stimulus and monetary versus fiscal stimulus are largely irrelevant in the face of institutional persistence that favors an existing order that by logic and any sense of social justice should have disappeared in 2008.

A new paper from J.W. Mason at the Roosevelt Institute joins the work of William Lazonick in tying modern finance to economic pillage by Western corporate executives that is emptying whole economies of productive capacity. Left largely unexplored in this research is the role of the Federal Reserve in this process. The Mason / Lazonick contention is that executives are using corporate resources to enrich themselves rather than to build ‘their’ companies. Before the 1980s forty percent of corporate earnings or borrowed money was invested in productive capacity—in future economic production. Today less than ten percent is with the difference going into the pockets of executives who borrow money on the corporate dime or use corporate earnings to raise the value of the stock options they have granted themselves.

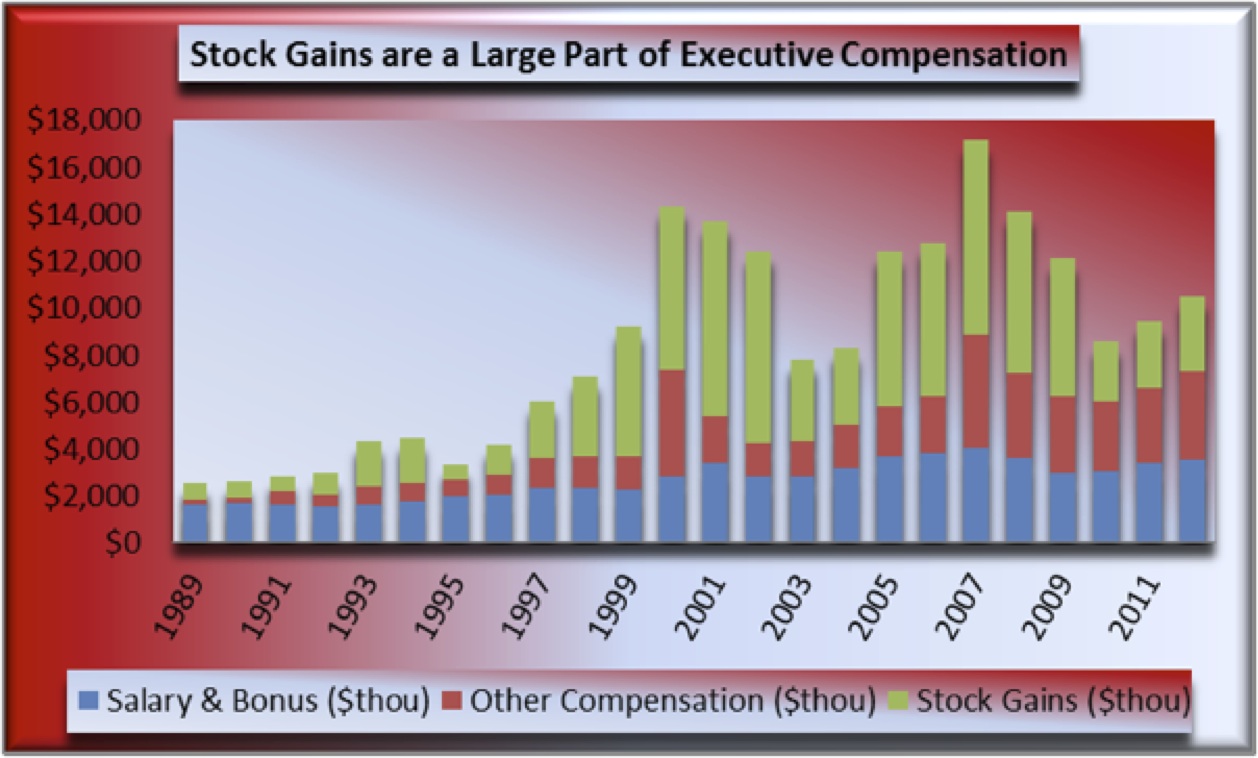

Graph (2) above: a substantial factor in the rise of executive compensation since the 1980s is the stock and stock options that corporate executives with compliant Boards of Directors grant themselves. Theory has it that ownership stakes give executives vested interest in corporate well-being. By using company earnings or borrowed money to buy-back stock executives raise the stock price and with it, their own compensation. This comes at the expense of future production and a potentially destabilizing increase in leverage. The combined effect is a rigged stock market and a corporate class that is gutting the broad economy for its own self-enrichment. Source: Forbes.

The Federal Reserve’s monetary policies since 2008 have been premised on theories of how companies and households make spending and investment decisions. Interest rates are the ‘price’ of borrowed money— the lower the price the cheaper that borrowing money is. The premise is that cheap money spurs companies to borrow to invest in their businesses. Left apparently unconsidered is that corrupt insiders would load up ‘their’ companies with cheap debt to enrich themselves while gutting the productive economy. Mason and Lazonick argue that this is precisely what is going on. And for those who may have forgotten how radically corrupt Federal Reserve actions were in bailing out Wall Street in 2008, Matt Taibbi provides details here.

In addition to lowering short term interest rates the Fed used QE (Quantitative Easing) to lower longer term rates through large-scale purchases of longer dated assets. QE had the added effect of raising financial asset prices by reducing the available supply as I explain here and the Bank of England explains here. The main beneficiaries of rising financial asset prices are the rich who own most financial assets and corporate executives who grant themselves stock options. And central to this self-enrichment are low interest rates that allow companies to fund stock repurchases using cheap debt. This practice leaves a gutted, overleveraged corpse of an economy behind. It also explains the remarkable recovery in the fortunes of the 0.1%.

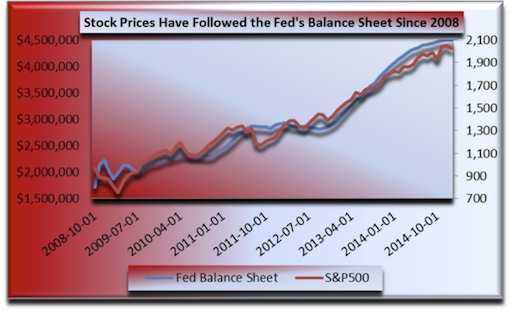

Graph (3) above: what mainstream economists call a conspiracy theory, the relation of QE to the rise in financial asset prices, was common knowledge on Wall Street within weeks of its inception in 2009. In addition to the ‘portfolio balance channel’ explained by former Fed Chair Ben Bernanke here, stock repurchases funded with cheap debt by self-dealing corporate insiders worked to tie the rise in the Fed’s balance sheet to rising stock prices. Articulation of the ‘portfolio balance channel’ makes it clear that Mr. Bernanke intended to raise financial asset prices with QE— it wasn’t an unintended consequence. Source: St. Louis Fed.

With the ECB (European Central Bank) set to commence its own QE program next month it is important to understand that both this program and the U.S. Fed’s have global consequences. Financial asset markets and global banks care little about the source of demand for financial assets making national and regional boundaries largely irrelevant to the effects of QE. In addition to gutting the productive economy by creating incentives to pillage, additional corporate and financial leverage makes the global economy more crisis prone by increasing cross liabilities and by raising the impact of any rise in interest rates. As was demonstrated in 2008 and continues to this day, the impact of bad and / or corrupt institutional policies falls most heavily on people who saw no benefit from them.

I have some sympathy for the argument that QE may not be optimal but that it is better than nothing. In this view it is irrelevant if corporate insiders enrich themselves as long as some benefit accrues to the broader populace. Also, in this view it is an accident of history that austerity economics re-emerged in Washington, London, Brussels and Frankfurt to make fiscal policies that would directly benefit this broader populace improbable leaving monetary policies that overwhelmingly benefit the already rich as the only remaining policy option. Back to Gramsci, and with relevance to events unfolding in Greece, in what way are these policies not in the service of the existing order alone? And what is the relevant time frame for measuring the claimed benefit, the time between crises or from one crisis to the next?

When Bill Clinton entered office as President in 1993 his chief economic advisor and ex-Goldman Sachs executive Robert Rubin ‘broke the news’ that the Federal budget deficit was larger than they had expected. This led Mr. Clinton to renege on his campaign promise of increased social spending. As a former banker Mr. Rubin well knew, or should have known, that the budget deficit bore no relation to the capacity of the Federal government to increase social spending. Consider this: a few short years after Mr. Clinton left office his successor, George W. Bush, dropped three-trillion dollars on a war of choice in Iraq. As with debate around monetary policy today, the frame that was brought to bear then was largely irrelevant to the institutional facts.

The theoretical frame that supports Federal Reserve (and IMF and ECB) policies works by compartmentalizing causes and effects. The contention that elite self-enrichment is either a market outcome or is socially neutral leaves aside the mechanisms used and the broader effects. The Federal Reserve has always based its policies on banker economics, on ‘managing’ Western economies to protect the value of bank assets from inflation. The result is that economic life is now substantially arranged around what supports Wall Street’s interests. This can be seen across the global periphery framed by class interests and supported by institutions like the Federal Reserve under the guise of social neutrality. Western economists serve the role of professional apologists in the service of these class interests. What is relevant to social resolution is the redistribution of political and economic power. This appears to be well understood by the looting classes who have so well redistributed it into their own pockets.

Rob Urie is an artist and political economist. His book Zen Economics is written and awaiting publication. A sampling of Rob’s art can be found here.