GDP grew at just a 2.0 percent annual rate in the third quarter as supply chain issues hampered growth in several key areas. Durable goods consumption contracted at a 26.2 percent annual rate, knocking 2.7 percentage points off the quarter’s growth. Equipment investment fell at a 3.2 percent annual rate, while housing construction dropped at a 7.7 percent annual rate, knocking 0.18 percentage points and 0.38 percentage points off the quarter’s growth, respectively.

Even with Third-Quarter Declines, Vehicle Consumption Is Still Far Above Pre-Pandemic Levels

The drop in third-quarter car sales accounted for 2.39 percentage points of the hit to GDP from durables. However, car sales are still 4.3 percent above the year-round average for 2020. This means that the supply chain problems are stemming from extraordinary demand, which will fade in the quarters ahead, not an inability to supply a normal quantity of vehicles.

Housing Is Also Above Pre-Pandemic Levels, In Spite of Third Quarter Decline

Even with the 7.7 percent drop in housing construction, which followed a drop of 11.7 percent in the second quarter, output in the sector was still more than 10 percent above the 2019 average. It will likely remain somewhere near the current level in future quarters, after jumping sharply due to low interest rates at the start of the pandemic.

Consumption of Services Grew at a 7.9 Percent Annual Rate in the Quarter

In spite of concerns about the spread of the delta variant, services grew at a solid 7.9 percent annual rate following growth of 11.5 percent in the second quarter. However, service consumption is still 1.6 percent below its pre-pandemic level. Recreation services and transportation, which is largely commuting expenses, account for the bulk of this drop. The category of food services and accommodations rose at a 12.4 percent annual rate in the quarter (in spite of delta) adding 0.54 percentage points to growth. Real restaurant sales are actually above pre-pandemic levels.

Inventories Added 2.07 Percentage Points to GDP in the Third Quarter

This was all due to growth in non-farm inventories, which added 2.14 percentage points to growth. Farm inventories continued a fall that began in the third quarter of 2015. The drop in farm inventories presumably is the result of both relatively low prices over this period and weather conditions. It is important to realize that inventories still declined at a $77.7 billion annual rate in the third quarter, but this was still a positive for GDP since it was much slower than the $168.5 billion rate of decline in the second quarter. As inventories stop shrinking and start to rebuild, they will be a big positive for growth in future quarters.

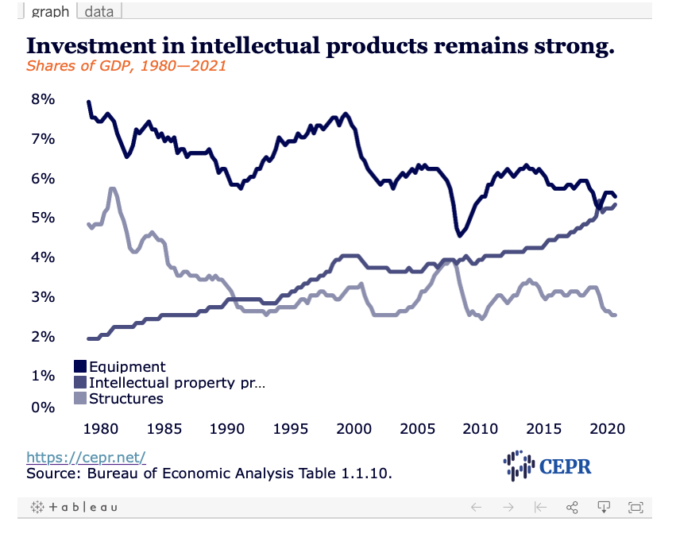

Nonresidential Investment Grew at a 1.8 Percent Annual Rate

Declines in equipment investment and structures largely offset an increase of 12.2 percent in investment in intellectual products. The rise in investment in intellectual products was the fourth consecutive double-digit increase. The 3.2 percent decline in equipment investment is likely due to supply chain problems, as it had been growing at double-digit rates for the last four quarters and orders remain high. The drop in structure investment is due to less demand for office and retail space, which is likely to be a permanent feature of the post-pandemic world.

Trade Deficit Subtracts 1.14 Percentage Points from Growth

A rise in the trade deficit, due to a 2.5 percent drop in exports and a 6.1 percent rise in imports, slowed growth by 1.14 percentage points in the quarter. The rise in imports was all on the service side, which rose at a 44.4 percent annual rate. This was largely US travel abroad, which was up more than 50 percent from the second quarter rate but still less than 60 percent of pre-pandemic level. Foreign travel in the US fell slightly in the quarter and is still just over 30 percent of pre-pandemic levels.

Saving Rate Remains Above Pre-Pandemic Levels

The saving rate was 8.9 percent in the quarter, which is well above the 7.5 percent average for the three years before the pandemic. This means that we are still not seeing the story pushed by inflation hawks that people would be spending down the savings they had accumulated during the period where large sectors of the economy were shut down, and they were getting the pandemic checks from the government.

Inflation and the Path Forward

The core Personal Consumption Expenditure (PCE) rose at a 4.5 percent annual rate in the third quarter, down from 6.1 percent in the second quarter. We are likely to see further slowing inflation as the supply chain problems get resolved in the quarters ahead. Shipping costs will be leveling off, so they will no longer be adding to inflation, and then dropping. It is important to recognize that the profit share of income rose sharply in the last two quarters, which means that rising prices have not been driven by higher labor costs.

This analysis first appeared on Dean Baker’s Beat the Press blog.