Regular readers of the leftish press have recently been presented with a raft of pleas coming from intelligent and occasionally articulate economists that the Federal Reserve not to raise interest rates. The general point being argued is that interest rates are the price of borrowed money, that raising them serves as a regressive tax because poorer borrowers pay a higher percentage of their incomes in interest expense than do rich people, and that the economy is still not fully recovered and higher interest rates risk sending ‘it’ lower again. Aiding the effort is the general loveliness of the people making the pleas versus the pissed-white-guys-in-suits contingent of monetary cranks who hate everything that the Federal Reserve does on the opposing side.

However, a wrinkle in the veil of loveliness can be found in ambiguity around the stated issues from none other than the Federal Reserve. The Federal Reserve is aware of the arguments of loveliness and is now wavering ever-so-slightly in raising rates only because a few stock markets have quite righteously shat the bed. Unless one conflates financial crapola with ‘the economy,’ a conflation the forces of loveliness insist is not warranted, then the Federal Reserve is now ambiguously poised to do the wrong thing for the wrong reasons (says the loveliness choir). The fact that all that the Federal Reserve seems to care about is ever-rising stock prices would seem to beg the question of why the forces of loveliness read so much more into the power of interest rates?

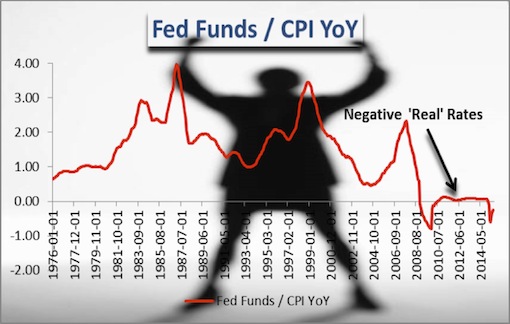

Graph (1) above: the faux Keynesian argument that ‘nature’ has an interest rate that ‘it’ prefers, the natural rate, is taken to infer that in certain economic depression / severe recession conditions this interest rate is negative. Negative interest rates ‘pay’ people and corporations to borrow money so that they buy things and produce goods. An alternative strategy that works directly is to have the government buy goods from corporations and give people jobs. The alleged goals are exactly the same, only one works directly and the other works with the ‘help’ of Wall Street. Guess which of these liberals and progressives have spent the most energy calling for over the last eight years? Units are ratio point change. Source: St. Louis Federal Reserve.

While understanding the minutiae of economic policies can sometimes seem daunting, evidence of plausibility, or its opposite, can often be found in the plainer words of economists. Ben Bernanke, the former Chairman of the Federal Reserve, developed the idea of a ‘global savings glut’ where trade surpluses found their way into subprime mortgages and arcane financial instruments in the U.S., Germany and France. Years after the term was used to explain the dotcom and housing booms and busts it is again being trotted out to explain financial bubbles in China, house prices in Manhattan and San Francisco and global stock and speculative bond prices. One potential setback for the theory is that the horse’s mouth from which it emanated, Mr. Bernanke’s, says it’s nonsense:

“The U.S. housing boom and the bust that followed resulted from the interaction of a wide range of factors, including problems with the originate-to-distribute model for mortgage loans, a deterioration in loan underwriting standards, deficiencies of risk management among financial institutions, contradictions in the incentive structures of the government-sponsored enterprises (GSEs), and problems in the scope and implementation of financial supervision and regulation….” Ben Bernanke et al (link below).

“To be clear, in no way do our findings assign the ultimate causality for the housing boom and bust to factors outside the United States. Domestic factors, including those listed in the first paragraph (quote above) of this paper, were the primary sources of the boom and bust and the associated financial crisis.” Ben Bernanke et al, 2011. Parenthetical added.

Getting to the heart of the matter may seem unduly esoteric and hard work-like. But the question is important to those who favor regular meals and living indoors: is the series of financial cum economic calamities of the last forty years an accident of nature or are specific policies, trajectories and actions causing them? The reason, I would speculate, that Mr. Bernanke persisted with the ‘global savings glut’ thesis is that it deflected culpability away from the Federal Reserve for the serial calamities it is both contributing to and overseeing. And the ‘global savings glut’ is once again being used to deflect culpability away from Central Bank policies. There is nothing like seeing the bomb that one has helped construct beginning to go off to focus the mind on strategies of plausible deniability.

The assertion that interest rates are the appropriate mechanism to support the poor and dispossessed requires fobbing off the question of precisely how they got poor and dispossessed. Black wealth was substantially stolen in the late 1990s and early 2000s by predatory mortgage lenders given free reign by the Federal Reserve and national and state regulators. Food insecurity as evidenced by food stamp (SNAP- Supplemental Nutrition Assistance Programs) usage more than doubled between 2000 and 2015. Employment security has plummeted as evidenced by workers aged 25 – 54 not in the workforce. Federal Reserve support for financial markets has increased poverty, not reduced it. And a look back at the recent history of Federal Reserve policies finds evidence of a singular goal: to support stock prices for the richest 1% of the population that owns stocks.

Graph (2) above: illustrates the rise and fall of the Federal Funds rate, the interest rate controlled by the Federal Reserve, in response to fluctuations in the stock market (Wilshire 5000). The participation rate of prime age workers and median family income were both in extended down-trends when the Federal Reserve began aggressively raising interest rates in 2005. Its reason for doing so then as well as threatening to do so now is the development of conspicuous financial bubbles— it had nothing to do with robust economic recovery increasing inflation. The punchline is that the last two times that the Federal Reserve raised interest rates financial markets crashed. Stock Market units are percent change (left scale). Fed Funds units are point change (right scale). Source: St. Louis Federal Reserve.

Precisely how damning Mr. Bernanke’s comments are (quotes above) probably isn’t apparent without being made so. By limiting responsibility for the housing boom and bust to domestic forces what is being said is that trade surplus flows had nothing to do with it (the ‘global savings glut’ thesis). If domestic U.S. ‘factors’ were responsible, the question becomes of where the money came from to blow the housing bubble? In fact, while BIS (Bank of International Settlements) research tends to be as spotty and self-serving as the Federal Reserve’s, two BIS analysts did a pretty good job of answering the question in 2011. Wall Street— large U.S., German and French banks, created the cheap leverage that encircled the globe from the low interest rates provided by the Federal Reserve.

The ‘global savings glut’ thesis is an effort by the (ex) Chairman of the Federal Reserve to blame ‘emerging markets’—countries and peoples on the receiving end of predatory Wall Street and IMF policies for most of the last half-century, for the plight of the tens of millions of people in ‘developed’ countries who lost their homes, jobs and life savings in the financial – economic debacle begun in 2007. Aside from the problem of scale asymmetry, Mr. Bernanke is either dissembling or lacks the requisite subject knowledge to hold his job with the thesis. Persistent trade imbalances like that of the U.S. (and its trading ‘partners’) result from policy choices, not ‘nature.’ And while it would be quite American to have a Chair of the Federal Reserve who has no idea of how the money system works, Mr. Bernanke isn’t that guy— and he’s making sure that we know it (quotes above).

U.S. trade imbalances are at their highest level a function of price, U.S. dollar exchange rates. The ‘strong’ U.S. dollar has favored (low cost) imports over (high cost) exports for some decades now. If trade flows determined the price of bank reserves then the ‘global savings glut’ theory might have explanatory power. But Mr. Bernanke says his own theory is nonsense (quotes above) for a reason. Banks make loans and then go looking for reserves. The Federal Funds rate is the price of bank reserves. A low Federal Funds rate provides low cost reserves for banks to leverage into loans. This is why the lovely people argue for a low Federal Funds rate.

The BIS paper (link above) adequately argues that gross capital flows (Wall Street money) overwhelmed trade surplus flows to create economic instability and that they were, circa the late 1990s, early-mid 2000s, a distinctly ‘developed’ market phenomena. Mr. Bernanke concurs by default in the quotes (with link to source) above. U.S. strong dollar policy is premised in the neo-imperialist conceit that growth of global capitalism centered in, and ‘managed’ by; the U.S. is in its long-term interests. Furthermore, currency exchange rates are relative prices and efforts at unilateral devaluation have a long history of fostering competitive devaluations.

The reason why Wall Street was pushing predatory loans in the run-up to the housing bust was because it could charge higher fees and ‘net-interest,’ the difference between what banks pay for reserves and the interest rate they charge on loans. In the later stages of the housing bubble many, if not most, of those borrowing to buy houses ‘qualified’ for lower cost loans but were ‘offered’ high cost loans— the cheap money that the banks were receiving had no bearing on the cost of the loans that they made. Since the housing bust similar bifurcated (class-based) lending has created a ‘tale of two recoveries’ where the high-priced houses of the rich are back in bubble territory while lower-end housing remains deeply ‘under water,’ worth far less than the mortgages owed against low-end houses.

Where all of this clutter and confusion comes clear is that the U.S. has the capacity to solve ‘aggregate demand’ shortfalls, whether caused by international trade (outsourcing of jobs) or scurvy-assed bankers looting their way to their fourth house in the Hamptons, by buying stuff and giving people paying jobs with benefits. The argument from the lovely people is that fiscal policies— having the government buy stuff and give people jobs, are not politically feasible. But why this might be true? Fiscal policies directly help the poor and unemployed while monetary policies directly benefit Wall Street and only occasionally and indirectly help anyone else. In a political environment where money rules, do policies that make the rich richer really benefit the ‘lower’ classes?

Graph (3) above: the monetary policies deemed politically feasible have been the only policy responses to the financial cum economic crises of increasing depth and breadth of recent decades. The trend lower in employment and median incomes has continued unabated as the rich who have benefitted from rising financial asset values have seen their circumstances made ever better. The ‘zero lower bound’ argument that Federal Reserve policies are limited because policy interest rates can’t go below zero (pay people to borrow money) was nowhere to be found when incomes and employment were declining in the early 2000s. What low interest rates did do then was to blow the most destructive financial bubble since the Great Depression. Yet more of the same is all that the contingent of lovely economists has to offer. Source: St. Louis Federal Reserve.

Most of the lovely economists are no doubt sincere in their belief that in weak economic conditions low interest rates benefit poor and working class people. But cracks emerging in the global financial and economic ‘architecture’ suggest another less benevolent reason for arguing for low interest rates. Another, and I would argue inevitable, global financial and economic crash would soon follow any move by the Federal Reserve to raise interest rates. Two decades of low rates are now, as they were in 2007 – 2008, built in to this architecture. Economic instability is the central and determinant feature ‘recovered’ since the crash of 2007 – 2008. Whether it comes from a ‘private’ credit induced crash in China and / or a leveraged commodities crash in the U.S., the poor and working classes are already set up to pay the price, no matter the cause.

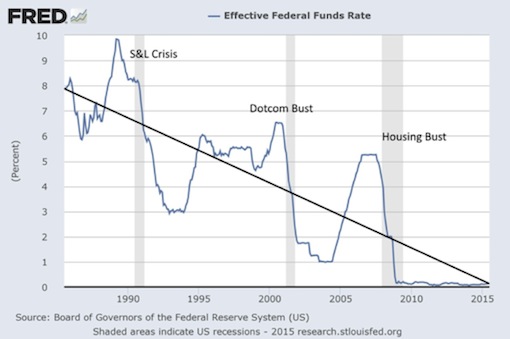

Graph (4) above: When Ben Bernanke argues (quotes above) that the housing boom and bust involved a host of factors he has a point, but not one that puts the Federal Reserve in a good light. Sequential interest rate movements lower have supported an increasingly destructive system of financial speculation and predatory lending. The S&L Crisis was created by a group of connected insiders looting a deregulated regional banking system. The Dotcom Bust was created by a group of connected insiders monetizing government-funded technology for their own benefit. The Housing Bust was created by a group of connected insiders looting the housing stock for their own benefit. The ‘public interest’ that drove Federal Reserve policy in these serial calamities was restoration of the system of looting with no apparent regard for the social carnage its actions were causing. Source: St. Louis Federal Reserve.

At this point in history the sole role of Wall Street is to set the metaphorical house on fire to collect the insurance money. Perpetual cheap credit and the unwillingness of the political class to act in the public interest by turning banks into heavily regulated public utilities has led to serial economic calamities of increasing scope and scale. Had Wall Street been resolved in any of the prior crises the forces of loveliness could more plausibly put their policies forward under the claim of pragmatism. However, Wall Street has only grown larger, richer and more powerful in each of these sequential crises. The social mechanisms are available to end it without economic calamity through a combination of fiscal policies and public banks created in the public interest. As things stand, the pleaders of loveliness are here to file the insurance claim forms when the house is inevitably once again set ablaze.

Finally, the question of whether cheap leverage or deregulation / the failure to regulate are responsible for serial crises assumes that the two are separable. In a narrow sense they are— the next crisis most likely won’t be driven by predatory home mortgages, just as the last wasn’t driven by a stock bubble (alone). But the ‘dislocations’ caused by predatory finance are accumulating with each new crisis. The unifying factor is Wall Street and the system of global finance it is metaphor for. ‘Reforms’ were made following each of the last three busts. But the problems have only increased in scope and scale. Add in dysfunctional state capitalism in China and looming global environmental catastrophe and either a different way is found or the crises will keep accumulating. Wall Street is a destructive diversion that should be ended and not kept on perpetual life support.