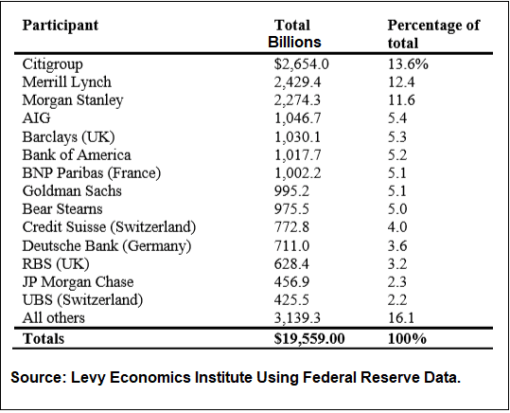

Largest Recipients of Federal Reserve Bailout Funds, 2007 to 2011.

From December 2007 to November 10, 2011, the Federal Reserve, secretly and without the awareness of Congress, funneled $19.6 trillion in cumulative loans to bail out the trading houses on Wall Street. Just 14 global financial institutions received 83.9 percent of those loans or $16.41 trillion. (See chart above.) A number of those banks were insolvent at the time and did not, under the law, qualify for these Fed loans. Significant amounts of these loans were collateralized with junk bonds and stocks, at a time when both markets were in freefall. Under the law, the Fed is only allowed to make loans against “good” collateral.

Six of the institutions receiving massive loans from the Fed were not even U.S. banks but global foreign banks that had to be saved because they were heavily interconnected to the Wall Street banks through unregulated derivatives. If one financial institution in this daisy chain of derivatives failed, it would set off a domino effect.

Another $10 trillion was spent by the Fed providing dollar swaps to foreign central banks, bringing the final tally of the bailout to $29 trillion. The Levy Economics Institute used the data that the Federal Reserve was forced to release through an amendment attached to the Dodd-Frank financial reform legislation in 2010 to compile the $29 trillion tab. Its figures are in line with the audit done by the Government Accountability Office (GAO), also mandated by the same amendment. The GAO audit included most, but not all, of the Fed programs, so its figures fall short of the comprehensive job done by the Levy Economics Institute.

There are two dark secrets about the Fed’s last bailout of Wall Street. First, the Federal Reserve Board in Washington, D.C., which is a federal agency with its Chairman and Board appointed by the President and confirmed by the U.S. Senate, outsourced the bailout to the Federal Reserve Bank of New York (New York Fed), which is a private institution owned by the Wall Street banks. The New York Fed, in turn, outsourced the management of the bailout to some of the very Wall Street firms that were receiving the funds. We know this from the details contained in the GAO audit. (See our “Vendor” section below.)

The second dark secret is that the underlying cause of the enormity of the bailout – hundreds of trillions of dollars in derivatives that interconnected the same global banks as counterparties – has never been reformed by Congress. A feeble attempt was made in the Dodd-Frank legislation but that was quickly repealed by an amendment forced into a must-pass spending bill by the largest recipient of the bailout – Citigroup, which was insolvent for much of the time the New York Fed was lavishing $2.65 trillion on it.

We know that derivatives are playing an outsized role in the current financial crisis because Wall Street banks, Deutsche Bank and the insurance companies (including AIG) that are still interconnected as derivatives counterparties are seeing their share prices bleed away to a far greater degree than the broader market indices. And, emphasizing our point, just last Friday as bank stocks were under trading pressure, the Federal Reserve announcedthat it was relaxing a rule on how the big banks would have to measure their counterparty credit risk derivatives contracts.

These same banks, as we write this, are currently receiving the next round of bailouts from the New York Fed, using many of the identical programs that the New York Fed used the last time around, like the Commercial Paper Funding Facility(CPFF), the Primary Dealer Credit Facility (PDCF), and the Term Asset-Backed Securities Loan Facility (TALF) along with a host of others. The goal of the New York Fed in using so many programs with so many alphabet-soup acronyms is to make it mind-numbingly difficult to keep track of the trillions of dollars it is spewing to Wall Street banks and their foreign peers. It took almost four years after the onset of the last unaccountable Fed money spigot to get accurate reports to the public about what it had done. The Fed spent more than two years in court battling to keep the public from learning the details.

How do we know that the same banks are receiving the new bailout funds? Because the New York Fed publishes a list of its 24 “primary dealers,” the Wall Street trading houses with which it conducts its open market trading operations and are eligible for its loans. (Yes, the New York Fed has its own trading floor – the only one of the 12 regional Fed banks to have one.) With the exception of AIG, which is an insurance company, Bear Stearns, which was taken over by JPMorgan Chase, and Royal Bank of Scotland (RBS), every bank listed in the chart above is currently eligible for the trillions of dollars in Fed loans that have been spewing out of the New York Fed since September 17, 2019 – four months before the first reported death from coronavirus in China and five months before the first reported death in the United States.

What makes the New York Fed’s bailout of Wall Street so much more dangerous this time around is that it has decided to use a different structure for its loans to Wall Street – one that will force losses on taxpayers and, it hopes, will provide an ironclad secrecy curtain around how much it spends and where the money goes.

The New York Fed plans to use Special Purpose Vehicles (SPVs) for many of its funding facilities again this time around. (It should provide no comfort to the American people that Enron used SPVs to hide the true state of its finances and blow itself up.) But last time around, the New York Fed put up the equity interest in the SPV and thus was on the hook for any losses.

This time around, the New York Fed is forcing the U.S. Treasury to put up $454 billion from the taxpayer to fund the equity stakes in its SPVs, which it plans to then leverage up to at least $4 trillion, according to White House Economic Advisor Larry Kudlow. But the New York Fed is then signing a private contract with a private Wall Street firm to allow it to be the manager of the SPV, handling the purchasing of toxic waste from Wall Street’s trading houses while funneling clean cash out to them. The New York Fed is asking these firms for an iron-clad confidentiality agreement that will, according to one we have read, survive the termination of the contract. The New York Fed has already set up three programs with BlackRock, one of the largest issuers of junk bond and investment grade corporate bond Exchange Traded Funds (ETFs).

The last time around, the New York Fed created the SPVs as Limited Liability Corporations (LLCs). Because the New York Fed had put up the equity interest in the SPV, under accounting rules it was considered to have a controlling financial interest in the SPV and had to consolidate the SPVs financial reports with its own. Those financial reports showed no granular details about who got the loans and the cumulative totals. Because it’s the taxpayer that’s putting up the equity interest this time around, there should be no such consolidated reporting or transparency at the New York Fed, except for those programs that are not SPVs, such as the Fed’s Discount Window. Discount Window borrowing details, under Dodd-Frank, are not released until two years later. The GAO audit that was released in 2011 told us this on the subject of the SPV LLCs:

“FRBNY [Federal Reserve Bank of New York] consolidated the accounts and results of operations of LLCs into its financial statements, thereby presenting an aggregate look at its overall financial position. FRBNY presents consolidated financial statements because of its controlling financial interest in the LLCs. Specifically, FRBNY has the power to direct the significant economic activities of the LLCs and is obligated to absorb losses and has the right to receive benefits of the LLCs that could potentially be significant to the LLC. While FRBNY’s financial statements include the accounts and operations of the LLCs, each LLC also issues its own set of annual financial statements.”

While only commercial banks have historically been allowed to borrow from the Fed’s Discount Window, the Fed invoked its emergency lending powers under the Federal Reserve Act and allowed its Commercial Paper Funding Facility (CPFF), which was structured as an SPV LLC, to borrow from the Discount Window. The GAO audit reveals this:

“The use of an SPV allowed FRBNY to leverage existing market infrastructure for the issuance of commercial paper. Using loans from FRBNY’s discount window infrastructure, the CPFF LLC would purchase eligible paper in the same way that investors would purchase this paper in the marketplace.”

The reason that the New York Fed had to become the buyer of last resort in the commercial paper market (and so many other markets) was because the Wall Street banks and their foreign brethren had become so interconnected with derivatives that none of them knew which firm might be the next Bear Stearns or Lehman Brothers and go belly up. So they simply backed away from rolling over each other’s commercial paper and other essential market functions. This is exactly what is happening today.

The New York Fed also used part of its $10 trillion in dollar swaps to help the Swiss central bank (a/k/a Swiss National Bank) set up an SPV to prop up UBS, the global bank with a huge footprint on Wall Street. The GAO report tells us this on the matter:

“…on October 16, 2008, the Swiss National Bank announced that it would use dollars obtained through its swap line with FRBNY to help fund an SPV it would create to purchase up to $60 billion of illiquid assets from UBS.”

The New York Fed’s “Vendors”:

According to the GAO audit, the New York Fed “awarded almost two-thirds of its contracts noncompetitively” for its bailout programs. JPMorgan Chase played an outsized role in many of these, including the Primary Dealer Credit Facility, where it doled out hundreds of billions of dollars in revolving loans to Wall Street trading houses, with junk bonds and stocks put up as a big part of the collateral. It was unprecedented in the 95-year history of the Fed at that time to be accepting junk bonds and stocks as collateral as well as unprecedented to be making loans to Wall Street trading firms. JPMorgan Chase also became the manager of the mortgage-backed securities that the New York Fed purchased as part of its QE1, QEII and QEIII programs. (See The New York Fed Has Contracted JPMorgan to Hold Over $1.7 Trillion of its QE Bonds Despite Two Felony Counts and Serial Charges of Crimes.)

According to the GAO audit, there was no contract between the New York Fed and JPMorgan Chase for its work on the Primary Dealer Credit Facility. The GAO says that the New York Fed simply “relied” on JPMorgan and another clearing bank, Bank of New York Mellon, “to execute transactions between FRBNY and program recipients (primary dealers). Agreements between the clearing banks and FRBNY identified eligible collateral and other program terms, but the clearing banks were paid by program participants and Reserve Bank officials did not know what fees the clearing banks were paid.”

An audit that doesn’t seek to learn how much JPMorgan Chase was paid as an incentive to award tens of billions of dollars to teetering firms such as Morgan Stanley against junk bonds and stocks as collateral – at a time when both junk bonds and stocks were plunging in price in the market – falls seriously short as a Government Accountability Office audit.

Other financial firms employed by the New York Fed that were revealed in the GAO audit included Morgan Stanley, PIMCO, and BlackRock, which it is using again today for three of its programs.

This article first appeared on Wall Street on Parade.

{kind=link}