Photo Source MAXmyd | CC BY 2.0

Off Balance Sheet Shenanigans in the Irish Financial Services Centre

Introduction

In November 2016, two of Russia’s largest banks MDM and B&N completed a merger. This new entity now ranked (by size of assets) in the top 10 of all Russian banks and the top 5 for private lenders. Following the merger CEO Mikail Shishkhanov declared, ‘We have laid the foundation for the creation of an international-class bank’.[1] Yet a mere 10 months later it required a bailout in what could be one of the mostly costly rescues in Russian banking history. [2] Mr Shiskhanov blamed these difficulties largely on MDM, whose losses ‘turned out to be much more serious than assumed in the conditions of a falling market’. [3]

How had those tasked with assessing MDM’s health prior to the merger failed to recognise such problems? Part of the answer lies 6000 kilometres away in the Irish Financial Services Centre (IFSC), via Ireland’s large shadow banking sector. Irish registered special purpose vehicles (SPVs), or shell companies in common parlance, have become widely used by Russian MNEs for off balance sheet financing and wider tax/regulatory avoidance. Between the years 2005-2016 around €110 billion was raised by Russian connected vehicles in the IFSC, [4] with Russian banks also using it as a location to hide losses. [5]

Concerned with the latter usage, this article examines MDM’s use of several IFSC based vehicles as part of a scheme that helped to create fictitious assets on its balance sheet, whilst simultaneously hiding losses. By providing loans to these off-balance sheet vehicles the bank was able to increase the size of its assets. These shell companies then used the proceeds to purchase some of the bank’s stock of non-performing loans (NPLs), thereby hiding some of its losses. An examination of the data contained in financial statements of MDM and its associated shell companies allows us to explore this insider dealing scheme, the techniques used to conceal what was happening and its effects on the bank’s balance sheet.

Background

The Russian Central Bank first approved the merger between the two banks in 2015, but negotiations had been on-going for several years previous. Up this point MDM had been struggling with a declining asset base and a rising level of NPLs. After reaching a highpoint of $13.3 billion in 2009, the size of its total assets went into sharp decline and had fallen to $10.6 billion by the end of 2011. So, with the bank shedding around $1 billion a year in value, a new chairman was appointed [6] coinciding with the creation of this scheme. Three IFSC based vehicles (Amaterasu Finance, Khepri Financeand Grengam Finance), and a fourth located in Malta (Juturna Limited) were used to form an extended corporate services supply chain, that could disguise the bank’s hidden hand in this insider dealing. [7] So how exactly did it all work?

The secrecy structure

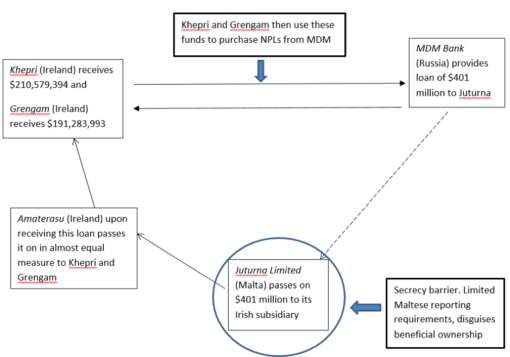

Beginning on the far right we can follow this funny money flow step by step.

Chart 1: MDM’s scheme

In 2012 MDM bank appears to have lent $401 million to the Maltese company Juturna Limited. Malta was likely chosen as the first link in this chain, as disclosure requirements in company accounts are minimal with the ‘ultimate beneficial owner’ not required to be on public record. Malta thus acts as the primary secrecy barrier disguising the linkage to MDM. Juturna’scorporate filings to the Maltese registry consisted on a single document, akin to an article of association, which contained no financial information whatsoever. It did however reveal that the international corporate service provider TMF Group were providing trustee and director services, just as they were to the three Irish vehicles. Interestingly enough on of these directors was mentioned in the ICIJ’s Offshore Leaks database.[8]

The Maltese company upon receiving the loan lent the proceeds to its subsidiary Amaterasu, which was the first IFSC based vehicle. Upon receiving the loan Amaterasu dispersed the funds in almost equal measure to the other two Irish vehicles Khepri and Grengam. Both vehicles used trust ownership structures to further obscure the relationship with MDM, and with a sufficient separation of ownership now in place, used the proceeds of the loans to purchase a significant amount of NPLs from the bank. Thus, MDM got back the money it had originally lent out but this time in the form of ‘new’ capital, which it received in return for the non-performing loans that were taken off its books.

Balance sheet implications

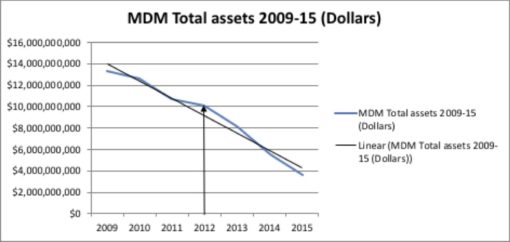

As we can see from the blue line in chart 2, MDM’s assets were in a state of significant decline. The $401 million loan in 2012 helped to partially arrest this decline (see linear line) allowing the bank’s assets to stabilise around $10.1 billion mark. Although such major problems could only be offset temporarily, especially considering the onset of the crisis in Russian financial system beginning in 2013.[9] Thus the three subsequent years saw this decline accelerate with the bank’s assets losing around $2.1 billion a year in value.

Chart 2: MDM’s total assets 2009-15

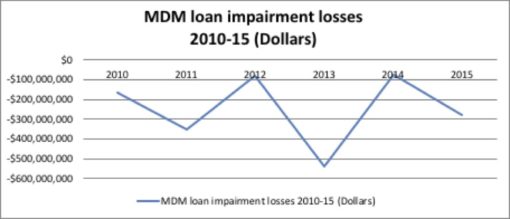

Similarly, if we look at the reported loan impairment losses on MDM’s balance sheet as displayed in chart 3, we see losses running at over $351 million in 2011. These losses fell to $80 million a year later after two of the Irish vehicles made their purchase of the NPLs. But again, this seemed to provide only a temporary reprieve as the losses rose to around $539 million a year later, before peculiarly falling again to around $75 billion in 2014 only to rise sharply again. The observable trend of peaks and troughs in chart 3, in addition to the numerous other OFC jurisdictions listed in the subsidiaries/affiliated entities section of MDM’s accounts [10], could be suggestive that the bank was also using other non-Irish off balance sheet for similar purchases of NPLs.

Chart 3: MDM impaired loans losses 2010-15

MDM had listed the par value of these NPLs as $1.1 billion, but after they were purchased by Grengam and Khepri for a discount they declined sharply in value until being written off in 2015/16. Amaterau’s loan had been written off the year previous. In total, these three vehicles reported losses of over $1.4 billion in the period 2012-16. The latest accounts of the Irish vehicles (2016) state they are all in the process of being wound up. Yet interestingly in July of this year two non-resident directors were appointed. One of currently whom serves as the deputy head of the International Bank of Azerbaijan’s London office, with the other stating he recently advised on a merger/acquisition.[11] Oh and still no word from the Maltese company whom Amaterasu defaulted on. Had this really been an independent company then we could have expected them to have started legal proceedings for the recovery of this debt

Conclusion

The above scheme seems to be a clear instance of insider dealing. MDM bank, through its use of Ireland and Malta, was able to exploit informational asymmetries that allowed it to carry out the above transactions. The difference between jurisdictions tax/regulatory/disclosure requirements provides the opportunity for corporates to engage in arbitrage. One possible antidote to these types of off-balance sheet schemes is public registries of beneficial ownership. Ireland has agreed in principle to the creation of such a registry, but it has now delayed its introduction until 2019, with the possibility of further delays. Until then it’s possible that banks will continue to hide losses in the shadows of the IFSC.

Notes.

[1]https://eng.binbank.ru/news/binbank-news/44812/

[2]The estimated cost of bailing out B&N bank along with Otkritie bank, another private lender which sought Central Bank assistance one month previous, is estimated to exceed $27 billion https://www.ft.com/content/72cb0ec4-4489-11e8-803a-295c97e6fd0b

[3]Financial Times (20/09/2017) accessed https://www.ft.com/content/5ecc58bc-9df7-11e7-9a86-4d5a475ba4c5

[4]Jim Stewart and Cillian Doyle (working paper 2018) ‘Ireland, Global Finance and the Russian Connection’ TASC seminar https://www.tasc.ie/download/pdf/ireland_global_finance_and_the_russian_connection.pdf

[5]For example the collapsed lender NBT bank had used a wide network of offshore vehicles spanning many jurisdictions, including Ireland, to hide losses. https://www.wsj.com/articles/hiding-russian-money-was-easy-quitting-was-harder-1533355260

[6]Igor Kouzine was approved by the board of MDM on the 1stof June 2012, source: https://www.marketscreener.com/MDM-BANK-PFD-9625112/news/MDM-BANK-PFD-Igor-Kouzine-Appointed-CEO-of-MDM-Bank-14353702/

[7]None of these vehicles appear in the subsidiaries/associated entities section of MDM’s accounts, and their use of nominee shareholders/trust ownership structures means consolidation was unlikely.

[8]Nadine Cacharia, ICIJ Offshore Leaks Databased.

[9]Anastasia Nesvetailova,The Offshore Nexus, Sanctions and the Russian Crisis https://www.iai.it/sites/default/files/iaiwp1524.pdfp.11

[10]The list of non-Russian subsidiaries in MDM’s accounts is drawn solely from other OFCs like Cyprus and Luxembourg.

[11]These two individuals Lala Huseynbayova and Muzaffar Usmanov. According to Lala’a Linkedin profle she currently operates as the deputy head of office of the IBA London branch, and formerly worked for the Azerbaijani embassy. https://uk.linkedin.com/in/lala-huseynbeyova-670aba8Muzaffar states he works for Four Oaks Advisory, is a former advisor to the First Deputy Foreign Minister of Tajikistan and advised HNWI on a merger/acquisition in 2015. https://uk.linkedin.com/in/muzaffar-usmanov-185a2720