In uncertain economic times, austerity is oft prescribed as a panacea to a nation’s economic ills. International organisations, business groups, mainstream political parties and the media lead the cheer squad about nations needing to live within their means. To the person on the street, there is logic to it; in household finance, earning more than you spend is seen as prudent, therefore governments should follow the same formula.

The trouble is, if you have ever studied a reasonable mainstream version of economics, you would know that in uncertain economic times, governments need to go into deficit to sustain economic growth. Although the aforementioned groups would have you believe otherwise, this is not a radical notion. In fact, it is largely attributed to a stuffy product of the British establishment, the economist John Maynard Keynes and his concept of the circular flow of income.

The theory goes like this. In an economy, you have households and firms. Households sell their factors of production – land, labour, capital and enterprise – to firms who convert them into goods and services. In return for selling their factors of production, households receive income – rent, wages, interest and profit – which they use to consume the goods and services produced by firms. This process constitutes the real economy – the production and consumption of goods and services.

Now, as we know, not all income is consumed. Some household income can be saved and some is paid in taxes. Savings is held by the financial sector and taxation his held by the government sector. According to the theory, the financial sector takes these savings and loans it in firms, who use it to invest in capital goods – machinery and so forth – so they can produce more in the long run. Government takes taxes and spends it on programs that it sees fit – whether that be social welfare or the machinery of war.

It is important at this point to acknowledge that the financial sector and the government sector have a power within this framework which is not granted to households and firms – they both can create money. The financial sector does this by lending more than people have saved, the government sector can do this by virtue of owning the printing press. This allows both these sectors to pump more finance into the real economy than they are collecting, stimulating economic growth.

(It is also important to point out, that in Keynesian parlance, savings is not only that which is left over after deducting consumption and taxes, but includes the paying off of loans.)

If income earned by households is the same as consumption, investment and government expenditure, then, at least in the short term, you have an economy at equilibrium – a steady state. Therefore, to attain economic growth in the short term, you do need some injection of new finance into the system. This encourages the production of more goods and services, and, if one takes a materialist point of view, thus improves people’s quality of life.

It was the Great Depression of the 1930s that spurred the development of this theory. Injections through investment had dried up as firms lost confidence that an increase in investment would generate enough return (and they were probably right, see Marx, K. on the tendency for the rate of profit to fall). Therefore, the government needed to ramp up its spending to make up for the lack of private demand (austerity had previously been tried as solution with dismal results). With the aid of a World War, this program of government spending pulled the economy out of its malaise and ushered in the 20th century’s “golden boom”.

This brings us to our original question. If history is any guide, in times such as these, government expenditure should be the go-to to drive economic growth. Why, then, do people, who should know better, advocate an austerity program which has failed in the past? Part of the answer is the rules have changed.

Why Austerity? Part II

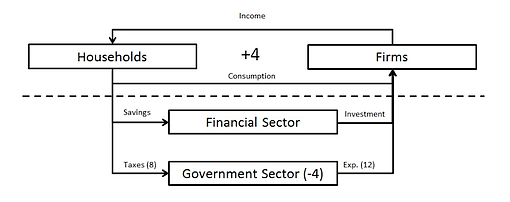

According to Keynesian economics, in an economy, there are four sectors (five if you count the external or overseas sector), households, firms, the financial sector and the government sector. Households and firms make up the real economy – the production and consumption of goods and services. The financial sector and the government sector can drain money away from the real economy through saving and taxes and they can inject it back in through loans for investment and government spending programs.

These two sectors, then, have a high degree of control over activity in the real economy. To demonstrate, say if the government sector collects 8 in taxes and spends 12 (this is the government which is allegedly living beyond its means). The government sector is in deficit by -4. That money has not disappeared, but is in fact an addition to private sector activity. So the government sector is in deficit by 4, but households and firms are up by 4.

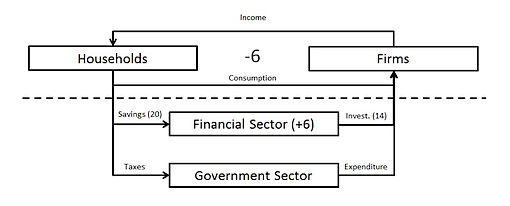

The same goes for the financial sector. If more is being saved than is being invested – say 20 is being saved and 14 is being invested, then the financial sector is in a surplus by 6, meaning the private economy is in deficit by 6. This financial sector surplus and private sector deficit phenomenon is what happened during the Great Depression.

So with business investment currently sluggish – companies like Apple are reportedly hoarding cash – why are so many preaching the need for government austerity? Surely, the logical thing to do in these times is for the government to run budget deficits, not surpluses.

As we have seen, if the government runs a surplus, this acts as a drain on the private economy. A surplus of 4 in the government sector will mean a deficit of 4 in the private economy. Faced with a deficit in the private economy, what do households need to do to maintain their standard of living? They need to obtain the finance from somewhere, and if it is not coming from the government sector, it can only come from the financial sector.

Running government surpluses means that people have to borrow from the financial sector. You do not have to be Adam Smith to see that the self-interest of the financial sector and their networks might be a motivating factor behind the drive for austerity.

By encouraging government surplus, the financial sector becomes the sole mediator of the economy. It decides how money will be spent – usually by pumping up asset prices rather investment for real production, which would improve people’s standard of living, as well as loans for things which were formerly covered by the government’s social spending, such as healthcare and education.

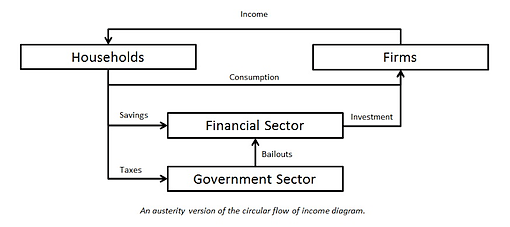

The financial sector does continue to see a role for the government, however. Given its exclusive license to print money, the government’s sole job is to bail out the financial sector when its investments (such as loans to people who can’t afford to repay them) turn bad (this process has also been called quantitative easing).

Ultimately, the losers in this process are the households, particularly those who depend on labour for income, who end up paying to prop up the financial sector. They pay “savings” to the financial sector in return for loans to maintain their standard of living and they pay taxes to the government in order to ensure they need to borrow from the financial sector. All the while the financial sector is not doing much except inflating asset prices to ensure that loans are needed for necessities such as housing, rather than productive investment and financing services that were formerly guaranteed by the state.

Note: For the sake of simplicity, I have not altered the circular flow diagram to account for its numerous other flaws, which include:

1/ As mentioned previously, savings is not exclusive to savings in the everyday sense of the word, but also includes repayment of loans.

2/ “Households” includes all groups who sell their factors of production such as labour and capital. Of course, the circumstances of someone who is predominantly an owner of capital and someone who depends on labour for income are vastly different. Even within the category of labour, the difference between skilled labour and unskilled labour is significant. Also, those with no factors of production to sell, such as the elderly or those with significant disabilities are not accounted for.

3/ Investment in an economic sense is usually taken to mean expenditure on capital goods – goods which produce other goods (which is why the investment arrow goes to firms). As such, the diagram does not acknowledge that a significant proportion of financial sector “investment” goes to households to finance the purchase of – and hence increase the price of – unproductive assets, such as real estate – and other expenses.