It might seem peculiar to some people to talk about the ‘next’ global recession, given that it doesn’t feel like we ever really got out of the last one. Eight years on from the global financial crash we find that the global economy is still drowning in debt, and this new era of low economic growth, high unemployment and squeezed wages/conditions has somehow become normalised.

‘Secular stagnation’ is the description de jure of the global capitalist system’s inability to return to another bout of prosperity. But while our old friend Boom departed the stage some time ago, his unruly brother Bust is waiting in the wings, preparing to make an unwelcome return.

Well that’s according to some of the world’s major financial institutions which have been forecasting that 2016 will be the year of the next big global downturn. In the last fortnight the IMF reduced its global growth forecast to 3.1%, that’s a mere 0.1% over the threshold of what constitutes recession. While last month Daiwa – Japan’s second largest brokerage house – and Citibank both released reports in which they made a global financial meltdown in 2016 their baseline scenarios! Let that sink in for a minute; they’re not saying a meltdown next year is their worst case scenario, they’re saying it’s their assumed one!

So what could trigger this predicted crash? Well to echo the words of Yogi Bear, ‘It’s tough to make predictions, especially about the future’. Nevertheless there is general agreement that debt was the trigger for the crash of 2008. Considering that today the global economy is even deeper in the debt mire, it requires no great leap of faith to believe that debt will be central to the coming crisis.

But let’s try narrow the focus a bit to the three main black spots where debt fuelled trouble is likely to emerge.

* Corporate debt: Despite the mainstream media’s constant scare mongering about government debt, its corporate debt we should be worried about. Corporate debt levels have ballooned to the point where a number of large multinationals, those big enough to be of systemic risk, look in danger of default. And should one collapse, we could be looking at another Lehman Brothers type moment.

* Stock market bubble trouble: Despite poor levels of economic growth over the last few years, massive bubbles have been building in global stock markets – fuelled by QE and low interest rates – with many now seemingly on the brink.

* The great Chinese slowdown: Despite mitigating the worst excesses of the 2008 crash through their massive stimulus measures, China’s engine is fast running out of steam. This has already hit commodity traders hard and pushed some emerging markets into recession. If it were to slip into recession itself it could drag the developed world down with it.

A Fate Worse than Debt

Do you remember ‘deleveraging’? Course you do, it was the great watchword of the corporate world in the post 2008 period. It’s essentially the process of selling ones assets to pay down debt. Well almost 8 years on, it’s safe to say it hasn’t happened, quite the opposite in fact, as corporate debt has hit new heights since 2008. With global growth continuing to decline and corporate profits starting to tumble, you can bet there are plenty of big multinationals who are looking at the liabilities on their balance sheets and then nervously over their shoulders.

One such corporate giant that’s been making headlines lately is Glencore. Glencore is one of the world’s largest commodity traders/mining operations, and its debt is looking more unsustainable by the day, with many banks and regulators worrying that its collapse could pose huge systemic risks. So how did it get here?

In the wake of the massive Chinese construction stimulus following the global crash, Glencore like many of the other mining giants, went hell for leather on cheap credit in an effort to expand their level of production to meet rising Chinese demand.

However with the major slowdown in the Chinese economy commodity prices are falling, meaning Glencore’s profits and share price have taken a serious hit. To make matters worse, it’s still tied to a multitude of what are now loss making mining contracts, which are costing the company berserk sums of money; meaning that it’s having serious trouble servicing its debt of around $30 billion.

What’s really frightening though is the insurance of Glencore’s skyrocketing debt, which the graph below illustrates. The Commonwealth Bank of Australia recently described Glencore’s trading division as ‘opaque’ and its exposure as ‘unknown’, which is coded language for; we don’t know what will happen if it collapses – but we know it will be bad.

This is reminiscent of Lehman Brothers, in that so much of their debt was tied up in exotic financial insurance instruments, and then repackaged and resold as other things like structured investment vehicles. Thus nobody really knew the extent of their exposure, so when they collapsed contagion spread like wildfire. Glencore’s current condition is starting to awaken many of those uncomfortable memories.

Graph 1.: CDS = Credit Default Swaps.

Bubble Trouble

Over the last few years stock markets have been bubbling away at a time when the global economy (China aside) hasn’t been able to get out of second gear. To the casual observer this might seem a peculiar state of affairs. For if a stock market (in theory anyway) is supposed to be a reflection of an economy and GDP growth levels are so sluggish, then clearly something else is driving this activity.

And that thing is debt. When we understand that a bubble is just the inflation of an asset – housing, bonds, stocks, etc – that is fueled by debt; and that governments and central banks have allowed debt levels to soar through quantitative easing (see: printing money) and low interests rates, then our story starts to make sense.

Instead of using the last few years to investment in productive things like research and development, large companies have been using their access to cheap credit to buy back their own shares, to increase dividends to their shareholders and to speculate in ever riskier financial instruments. All of which has served to fuel the kind of stock market bubbles that we can see illustrated below in the example of the US.

Graph 2.

This major debt overhang, coupled with the current climate of weak demand, is what stopped the Federal Reserve from raising interest rates in September, and it’s unlikely they’ll deviate from that policy at the end of the year. Because if they were to suddenly hike interest rates, many large companies who have become reliant on cheap credit just to maintain the day to day costs of operations would suddenly have a major problem servicing their debts, and such a jolt to the system could provoke a stock market crash.

This is what happened in the stock market crash of 1937, or as its often known as ‘the recession within Depression’. After a weak recovery from the Great Depression, where unemployment was still high, policy makers tightened fiscal and monetary policy as a pre-emptive measure against inflation – the effects of which proved devastating.

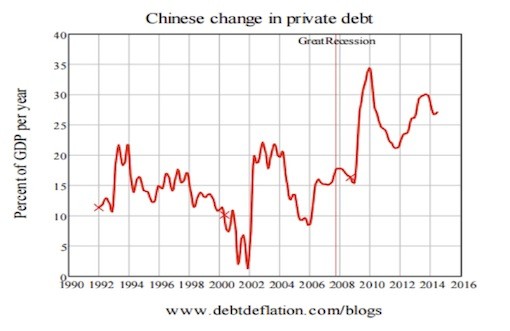

The great Chinese slowdown

The massive stimulus measures the Chinese government undertook after 2008 is what kept global demand from collapsing. So much so that in 2012 China managed to account for a whopping 85% of global growth. But they borrowed massively to fund this stimulus, meaning debt levels ballooned as one of the largest property bubbles in human history was created. The graph below should give an indication of why Chinese policy makers, fearing a bursting of this bubble, have sharply cut back on construction, therein seening their share of global growth fall to less than 25%.

The effect of this contraction has been twofold; internally the rapid decline in growth means that Chinese firms are now facing increased pressure to repay their debts. But as Zero Hedge described just days ago; a quarter of Chinese firms with debt are unable to cover their annual interest expenses, meaning the Chinese banks having a significant amount of non-performing loans, far higher than the figures being given out by China’s banking regulator.

Externally China’s contraction has had a detrimental knock-on effect for the other emerging economies (Russia, Brazil, Argentina, India, etc) that had been supplying them with their base commodities for construction. The drop-off in demand for such goods has seen these countries pushed back into recession or on its edge.

Compounding this problem is the fact that many of these emerging economies, just like their more developed counterparts, are riddled with debt. In recent years many of their largest corporations borrowed heavily in cheap dollars. However with the value of the dollar continuing to rise relative to currencies of these emerging markets, they have been left badly exposed to a hike in US interest rates. And for those who know their history, this is not unlike what happened in the early 1980s with the Latin America debt crisis.

China is unlikely to face the same kind of financial crises that befell its neighbours Japan and South Korea in the 1990s, or Britain and the US in late 2000s. Quite simply because much of its debt is owed by state owned companies, it controls its own banks and it has the means to bail them out. Furthermore it has vast foreign exchange reserves, so there’s no need to fret about foreing capital suddenly drying up.

However the problem it does face is one of a slow burn debt crisis. Using its banks to simply engage in pretend and extend, by providing continuous credit to state owned firms that are failing, could result years of deflation and stagnation.

A matter of life or debt

The global economy is heading for a fall. Debt continues to scale new heights, growth is in the doldrums, and our political masters are fast running out of options. In 2008 they could loosen monetary policy and print money but now they’ve played this hand, which has resulted in bubbles in global stock markets and more debt in a world already saturated with the stuff. Now with the massive slowdown in China and other emerging markets, the world is on the brink of slipping back into another global recession.

What’s needed now is something much more radical; something that tries to get to the heart of the problem. Considering that debt, and to be more exact private debt, has created one of the biggest bubbles in human history, which unsurprisingly proved to be the trigger for the last crisis, why not look toward a debt write off of biblical proportions?

Taking its inspiration from the book of Deuteronomy, some people have been advancing the idea of a modern debt jubilee. The rationale behind this is simple and sound, and is captured nicely by Michael Hudson’s quip that ‘debts that’s can’t be repaid, won’t be repaid’.

The unfortunate thing is that it will probably take another global financial meltdown before such an idea can start to gain real traction. But the ways things are going we shouldn’t have to wait too long.