President Joe Biden and Congressional progressives have responded to public pressure by putting bold spending proposals on the table that would make our economy more fair, sustainable, and resilient in the face of future crises.

The chances of these proposals passing depends largely on whether lawmakers can reach consensus around tax increases on wealthy individuals, big corporations, and Wall Street. The 11 charts below show how such reforms would both generate revenue to help pay for transformative public investments while also curbing the skyrocketing inequality that is undermining our society and democracy. According to Americans for Tax Fairness, such fair tax reforms are extremely popular, with voters expressing support by 60-65 percent or more in 12 recent polls.

Taxes on the Wealthy

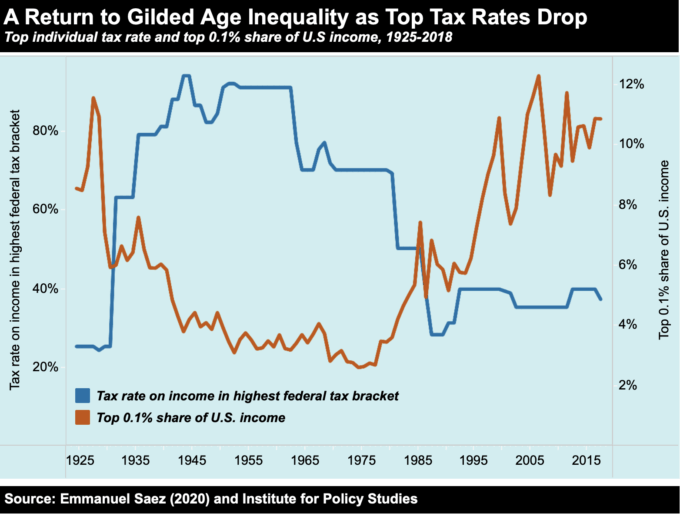

Biden aims to raise the top marginal tax rate from 37 percent to 39.6 percent, where it stood before the 2017 Republican tax cuts. Tax rate hikes at the top were an effective tool in reversing the extreme inequality of the “Gilded Age.” Under high top rates in the post-WWII decades, the share of national income flowing to the richest 0.1 percent fell significantly. When policymakers once again slashed those rates, beginning in the 1960s and accelerating in the 1980s, inequality shot back up. According to Professor Emmanuel Saez, the richest 0.1 percent of Americans pocketed 10.84 percent of total U.S. income in 2018, a level not seen since 1929. Contrary to the arguments of tax hike opponents, real U.S. GDP grew faster in the 1950s and 1960s than in more recent decades. The subsequent decade with the highest growth rate was the 1990s — after Congress enacted moderate top tax rate increases.

In the United States, wealth inequality is even more severe than income inequality, and the reduction in the top income tax rate has been a key factor. According to Institute for Policy Studies analysis of data collected by Saez and fellow economist Gabriel Zucman, the share of U.S. taxes paid by the top .01 percent was just slightly higher in 2018 than in 1962, despite the more than tripling of their share of the nation’s wealth. By contrast, the bottom 50 percent saw their share of U.S. wealth drop by more than half during this period. The top marginal tax rate in 1962 was 91 percent, compared to 37 percent in 2018.

Institute for Policy Studies analysis adds further evidence of the direct connection between tax policy and extreme wealth concentration. The rate of taxation of America’s richest .01 percent of households, as a percentage of their wealth, decreased by over 83 percent between 1953 and 2018. The decline in this relative tax rate accelerated after 1979. Stronger minimum wage, antitrust enforcement, and unionization rates during the 1953-1979 period undoubtedly had some equalizing effect, and yet during this period it required a top tax rate four times the current rate simply to keep the wealth share of the top 0.1 percent in check.

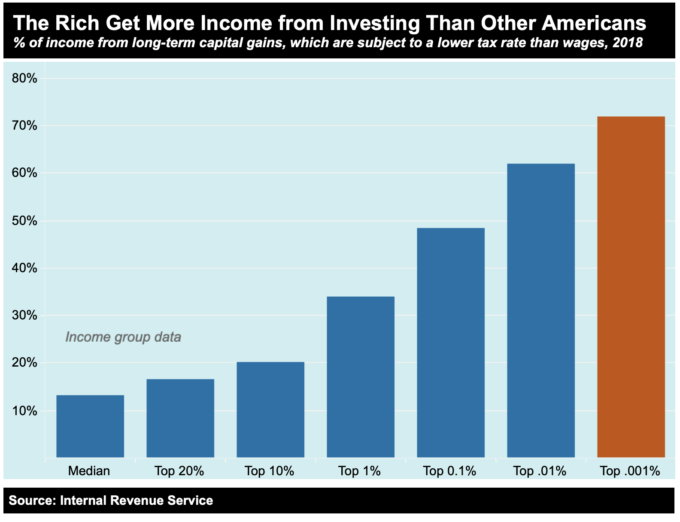

Why do the rich pay such a small share of total U.S. taxes, relative to their great wealth? Beyond their ability to hide their money from the IRS, the rich benefit from the tax code’s preferential treatment of income from investments. Currently, the top marginal tax rate for the richest Americans is 37 percent, while the top rate for long-term capital gains is just 20 percent. The higher the U.S. income group, IRS data show, the larger the share of income derived from investment profits. By contrast, Americans who are not among the ultra-rich get the vast majority of their income from wages and salaries.

The rich are well-positioned to benefit from the discount tax rate on investment earnings because of their dominance on Wall Street. Federal Reserve data indicate that the richest 1 percent hold more than half of all stocks and mutual funds, while the bottom 90 percent of Americans own just 11 percent. The disparities in stock ownership are even starker if race is factored in. While 61 percent of white families owned at least some stock in 2019, only 34 percent of Black and 24 percent of Latino families did, according to the Federal Reserve.

Biden’s plan would close the capital gains loophole for the rich by requiring individuals earning more than $1 million a year to pay the same tax rate on the sale of stock and other assets as they pay on income from wages.

America’s richest also exploit estate tax loopholes, shell corporations, trusts, and other sophisticated methods of shielding their accumulated fortunes from taxation. This has accelerated the accumulation of wealth — and power — in the hands of a few individuals while entrenching oligarchic dynasties. According to Institute for Policy Studies research, America’s 50 wealthiest family dynasties together held $1.2 trillion in assets in 2020. By comparison, the bottom half of all U.S. households—an estimated 65 million families — shared a combined total wealth of just twice that, at $2.5 trillion. The five wealthiest dynasties (the Walton, Koch, Mars, Lauder, and Cargill-MacMillan families) saw their wealth increase by a median 2,484 percent from 1983 to 2020.

The Biden plan would curb wealth concentration by strengthening the estate tax and closing a loophole that allows the wealthy to escape capital gains taxes altogether on assets they pass on to their heirs. Senators Bernie Sanders and Elizabeth Warren and other Democrats have also called for an annual wealth tax. Their proposal would raise an estimated $3 trillion over a decade by taxing fortunes worth more than $50 million at a rate of 2 percent and those with wealth of more than $1 billion at 3 percent. Institute for Policy Studies Associate Fellows Lee Price and Bob Lord have suggested a third tier of 10 percent on wealth in excess of $5 billion.

Taxes on Corporations and Wall Street

America’s wealthy have also benefited enormously from reductions in the corporate tax rate, which has fallen from a peak of 52.8 percent in the 1960s to 21 percent under the 2017 Republican tax law. The windfalls of lower corporate taxes flow primarily to high-income Americans because of their disproportionate ownership of corporate stock. Wealthy corporate executives, who receive most of their compensation in some form of stock-based pay, also benefit, while evidence of gains for workers is lacking.

This corporate tax rate-cutting, combined with rampant use of offshore tax havens and other avoidance schemes, puts a strain on public budgets. The percentage of total federal revenue from corporate tax receipts dropped from 32.1 percent in 1952 to 6.6 percent in 2019, according to Office of Management and Budget data.

Most Democrats agree on the need to increase corporate taxes, but views differ on the ideal rate. Biden has proposed an increase from 21 to 28 percent, along with a global minimum tax and other measures to curb offshore tax dodging. Senate Budget Chair Sanders would like to see a return to the 35 percent rate, while some moderates have proposed 25 percent.

As corporate tax obligations have declined, CEO pay has skyrocketed. According to Office of Management and Budget data and Economic Policy Institute research, when corporate tax receipts made up 21.8 percent of all federal revenue in 1965, the average CEO-to-median worker pay ratio was 21 to 1. After the 2017 Republican tax cuts, corporations plowed significant windfalls into stock buybacks and executive bonuses. By 2019, corporate tax receipts had fallen to just 6.6 percent of federal revenue and the average pay ratio had risen to 320 to 1.

Progressive senators and House members have introduced the Tax Excessive CEO Pay Act to incentivize corporations to narrow their economic divides. The bill would apply graduated tax increases on corporations with large CEO-median worker pay gaps, beginning with 0.5 percentage points on corporations with pay ratios of 50 to 1 and rising to 5 percentage points on firms with ratios above 500 to 1.

Opponents of raising the U.S. corporate tax rate often point to lower statutory rates in other large economies. But huge loopholes in the U.S. tax code have lowered the effective rate that corporations actually pay the IRS. In fact, the Institute on Taxation and Economic Policy found that 55 large, profitable U.S. corporations paid zero in federal income taxes in 2020. Because of these loopholes, U.S. corporate tax revenue as a share of GDP is actually lower than in any other G7 country. By contrast, average CEO pay at large U.S. corporations is off the charts compared to their international counterparts, according to Institute for Policy Studies analysis of Willis Towers Watson data.

Policymakers should not tie their hands by requiring every dime of new spending to be offset with new revenue, especially given the enormous long-term benefits of health care, education, and climate change investments. But there will be pressure to pay for a considerable share of new spending, and Biden’s total proposed corporate tax changes, including a global minimum tax and other loophole closures, would generate an estimated $2.2 trillion. This chart compares revenue from just one of Biden’s proposed reforms — an increase in the corporate rate from 21 percent to 28 percent — with the cost of select investments that would help American families fulfill their potential and live in dignity.

Ordinary Americans are used to paying sales taxes when they purchase a car or home, a tank of gas, or a restaurant meal. But when a Wall Street trader buys millions of dollars’ worth of stocks or derivatives, there’s no sales tax at all. This tax-free approach has also contributed to the explosion of the algorithm-based computerized trading that dominates our financial markets while adding no significant value to the real economy. Just one indicator of the disparity between these traders and low-wage workers: since 1985, the average Wall Street bonus has increased 1,217 percent. If the minimum wage had increased at that rate, it would be worth $44.12 today, instead of $7.25, according to the Institute for Policy Studies.

Lawmakers have introduced several financial transaction tax bills that would generate massive revenue while curbing short-term speculation. Under one proposal, a tax of just 10 cents on every $100 worth of trades in stock and other securities could raise some $750 billion over 10 years.

The raging debate over public investment financing has created a huge opening for long overdue fair tax reforms. Without drastic changes in the tax code, we will continue to see those at the top accumulate ever more obscene levels of wealth and power while our physical and human infrastructure crumbles and low-income Americans, particularly people of color, get left behind.

Sarah Anderson directs the Global Economy Project, Brian Wakamo is an inequality research analyst, and Justin Campos is a Next Leader at the Institute for Policy Studies.