The long-standing, loosely-woven patchwork of federal, state and local programs in the U. S. includes the emergency rooms and urgent care clinics of public hospitals, community health centers, and local health departments. Their goal is to serve a long list of vulnerable populations —uninsured and underinsured, chronically ill individuals, people with disabilities, mentally ill individuals, people with communicable diseases, legal and undocumented immigrants, minorities, native Americans, the homeless, substance abusers, and prisoners.1 Medicaid is the principal funding source for safety net care, but varies greatly from one state to another and is often inadequate to the needs.

This paper has three goals: (1) to give examples of how frayed the safety net is today; (2) to summarize the major barriers to establishing a solid and reliable safety net; and (3) to briefly describe what we have learned from attempted policy fixes in past years and what could be done today.

How Frayed Our Safety Net Is Today

Our completely unacceptable safety net, without any real improvement over many years, is the Achilles heel of an out-of-control health care system that leaves the word “care” out of its goals as it profiteers on the backs of patients, families, and even taxpayers as well. Dr. Jack Geiger, founding member and past president of Physicians for Human Rights and pioneer developer of community health centers, issued this challenge 20 years ago:

What we deal with in our work, quite apart from the extremes of genocide, is a variant of that: “Lives less worthy of life.” When we say that the poor have a mortality rate that is multiple times the rate of the rich, when we say that poor children die in our country and in the developing world at rates far higher than those who are better off, we are saying that we permit a condition which in effect says that they are less worthy of life. We are sending this message because we let it happen, because we have social politics that almost assure that it will happen, and we let it happen stubbornly and continually.1

Being “insured” is not a useful metric for tracking the value of the safety net, as shown by these markers of having no safety net while being insured:

+ Even after passage of the ACA in 2010, insurers still discriminate against insured patients by benefit designs that limit access, have high cost-sharing, restrictive drug formularies, and ever-changing networks of physicians and hospitals. They also market inadequate gap insurance that require copays for treatment of such conditions as cancer, heart disease and stroke,2 as well as very profitable short-term plans with very limited coverage up to 1 year that have come to be known as “junk insurance.”3

+ Denial of claims, even including emergency air transport through lengthy pre-authorization processes; 18 percent of claims denied in privatized Medicare plans.4

+ Women’s health care coverage is often limited in both private and Medicaid plans; as a result, women frequently skip essential care, a major factor in the U. S. having the highest maternal mortality rate among high-income countries (#46 in the world)5

+ As a result of increasing cost of premiums, four in ten people with employer-sponsored health insurance do not have enough savings to cover the deductibles.6

+ An Inspector General’s 2014 survey of 1,800 physicians listed on Medicaid managed care rosters found that a majority were unavailable for appointments.7

+ We have a chronically underfunded, limited access system for mental health care, with many mentally ill ending up in jail, where they receive little if any care.

+ Periodic cross-national studies by the Commonwealth Fund of 11 advanced countries consistently find the U. S. last for access, equity and quality of care.8

+ Even when insured, many enrollees receive high surprise medical bills that drag them into poverty that often leads them into medical bankruptcy.9

+ Private insurers often leave unprofitable markets with little advance notice, as they did at the end of 2016, when they left 1.4 million people in 32 states with fewer choices than before.10

+ Health insurers’ modus operandi is well summarized this way by Gerald Friedman, Ph.D., Professor of Economics at the University of Massachusetts Amherst and author of The Case for Medicare for All:

Health insurers profit by screening customers, segmenting the market so as to exclude those likely to use health care (“lemon dropping”) while attracting the healthy and lucky who use less health care (“cherry picking”). While profitable, such activities add to the cost of America’s bloated health care administration, raising a question that we should ask of all health insurers: how many patients did your company help today? 11

Chronic Barriers to Reform

These are some of the major barriers to achieving a national system of universal coverage with an intact safety net:

Leaving the issue of salvaging a safety net to the states.

Many states give Medicaid low funding priority while a growing number of Republican voters in southern states even favor secession over compromising with a Democratic administration.12 In these present polarized political times, states are diverging sharply on such issues as abortion and women’s reproductive rights, making any unified policy to build a national safety net beyond possibility.

Solid opposition from big business, corporate America, Wall Street stakeholders, and Chamber of Commerce with deep pockets and strong lobbying against reform.

As one example, leading insurance, hospital and pharmaceutical lobbyists have formed the America’s Health Care Future to defeat single payer Medicare for All through heavy lobbying and a targeted disinformation campaign.13Another example: A GOP outside group aligned with Senate Majority Leader Mitch McConnell (R-KY) launched a multi-million-dollar ad campaign against Medicare for All targeting legislators in both parties. With campaign contributions they spread doubts about Medicare for All; the chair of the Democratic Congressional Campaign Committee later said that its costs would be “scary.”14

With its profit-based business model, corporatization, profiteering, and private equity, the corporate controlled health care marketplace, as one-sixth of the nation’s GDP, is doing just fine without reform.

Its momentum to continue its grip on U. S. health care is illustrated by Amazon’s current plan to buy 1Life Healthcare, Inc, which operates a giant primary care practice with more than 180 medical offices in 25 U. S. markets.15

Lack of a public groundswell to reject the Citizens United decision while billionaires control election spending, which portends continuance of conservative barriers to reform in Congress.16

Lack of national commitment, public outrage, and collective moral responsibility to push to alleviate safety net losses by adopting a system of universal coverage.

Larry Churchill, Ph.D., and ethicist at the University of Notre Dame, brings us this perspective in his 1987 book, Rationing Health Care in America: Perceptions and Principles of Justice, as to the significance of what has happened for many years to the less fortunate among us confronted with their own health care:

A health system which neglects the poor and disenfranchised impoverishes the social order of which we are constituted. In a real (and not just hortatory) sense, a health care system is no better than the least well-served of its members.17

Lessons from Failed Policies and What Can Be Done Now?

We could well have learned as far back as 1944 that health insurance must be compulsory in order to eliminate segmentation of risk pools. As Dr. Henry Sigerist, then Director of the History of Medicine at the Johns Hopkins University said at the time:

Illness is an unpredictable risk for the individual family, but we know fairly accurately how much illness a large group of people will have, how much medical care they will require, and how many days they will have to spend in hospitals. In other words, we cannot budget the cost of illness for the individual family but we can budget it for the nation. The principle must be to spread the risk among as many people as possible . . . The experience of the last 15 years in the United States [since 1931] has, in my opinion, demonstrated that voluntary health insurance does not solve the problem of the nation. It reaches only certain groups and is always at the mercy of economic fluctuations . . . Hence, if we decide to finance medical services through insurance, the insurance system must be compulsory.18

Our public-private non-system of financing U. S. health care has become big business with the primary goal to make as much money as possible for CEOs and shareholders on the backs of patients and families. Corporate stakeholders and their well-funded lobbyists travel through the revolving door between industry, government and K Street to further their self-interest with little regard for the public interest.

Corporate stakeholders in the current non-system, with its widespread disparities and inequities, have been spreading disinformation to convince legislators and policymakers that a system of national health insurance would break the bank and be “socialism.”

As noted previously, the Institute of Medicine’s study of 20 years ago concluded that system changes then posed an increasing threat to the safety net. Unfortunately, these current and imminent changes today pose an even greater threat to the future of our safety net:

+ Increasing emphasis on states’ rights with wide polarization between major political parties.

+ Widening gulf between red and blue states with increasing sentiment for secession among voters in some southern states.

+ Rampant gerrymandering in some states with the electoral map in many states up for grabs in the 2022 midterms.

+ The U. S. Senate blocking progressive bills passed in the House whether by the 50-50 Senate membership by party or by the use of the filibuster.

Still missing in the public debate over U. S. health care is a sense of public outrage and collective moral responsibility to overcome corporate and political opposition to a system of universal coverage that could prevent so many millions of Americans from falling through a porous safety net.

Reform Alternatives under Current Consideration

With health care a front-burner issue as we head into the 2022 and 2024 election cycles, these four reform alternatives are up for debate:

1. Building on the Affordable Care Act of 2010;

2. Medicare for Some: lowering the age of eligibility for Medicare from 65 to 60, together with a public option for sale alongside private plans on the ACA’s exchanges;

3. Privatized Medicare Advantage for All; and

4. Single-payer Medicare for All

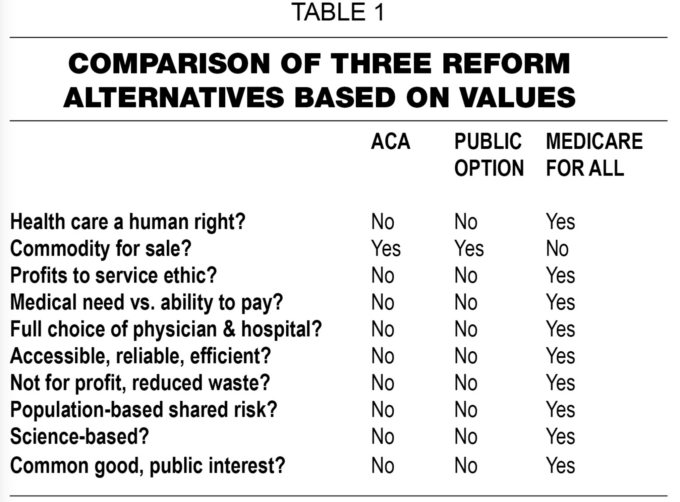

The first three of these options would leave in place a deregulated, for-profit, multi-payer financing system with all of its profiteering, wasteful bureaucracy, inequities, and unreliability. Since the 1990s, mergers and consolidation within the private health insurance industry have left the largest (in numeric order: United Health Group, Anthem, Aetna and Cigna) with a collective market share of 48%.19 That level of consolidation has brought more cost-sharing with higher deductibles, reduced access and utilization of care.20 Privatization of public programs has been especially profitable for insurers; as one example, most of United Health’s reported profits in 2021 came from its Medicare Advantage plans and state Medicaid plans without growth in their numbers of enrollees.21

The fourth alternative is the only one that can rein in health care costs, improve access and quality of care, and effectively build a solid safety net. (Tables 1 and 2)22

Medicare for All would usher in a new system of national health insurance for all Americans with comprehensive benefits based on medical need, not ability to pay. Its administrative overhead would drop to about 3 percent, about one-sixth of private insurers’ multi-payer overhead, without cost sharing at the point of service and with mechanisms to rein in profiteering. Had it been in place in 2019, it is estimated that we would have saved more than $1 trillion for the reasons shown in Figure 1.23

Conclusion.

Can we ever achieve a safety net that works for all Americans? Based on history, the odds are against it, but it should be possible for the wealthiest nation in the world that brags, incorrectly, that it has the best health care on the planet. Shifting from today’s business model to one of service can also help to re-establish traditional ethical norms of the health care professions. Perhaps we can learn from the history of our missteps over the last 110 years to find the necessary path forward. To that end, we can take hope from these words by Winston Churchill: “Americans will always do the right thing—after they exhaust all the alternatives.”

References.

1. Geiger, HJ. Why we do what we do, speech. Doctors for Global Health, August, 2002.

2. Silverman, RE. For workers, and “insurance on insurance.” Wall Street Journal, 2016: B 5.

3. Hiltzic, M. Why the short-term plans are cheap: They shortchange you on care. Los Angeles Times, 2019.

4. Silvers, JB. This is the most realistic path to Medicare for All. New York Times, October 16, 2019.

5. Gunja, MZ, Seervai, S, Zephrin, L et al. Issue Brief. Health and health care for women of reproductive age: How the United States compares with other high-income countries. New York. The Commonwealth Fund, April 6, 2022.

6. Levey, NN. Health insurance deductibles soar, leaving Americans with unaffordable bills. Los Angeles Times, 2019.

7. HHS Inspector General’s Report; OEI-02-13-00670, December 2014.

8. Schneider, EC, Shah, A, Doty, MM et al. Mirror, Mirror 2021: Reflecting poorly. New York. The Commonwealth Fund, August 4, 2021, p. 3.

9. Himmelstein, DU, Lawless, RM. Thorne, D et al. Medical bankruptcy: Still common despite the Affordable Care Act. J. Public Health, 2019: 109 (3): 431-433.

10. Tracer, Z, Darie, T. More than 1 million in Obamacare to lose plans as insurers quit. Bloomberg News, 2016.

11. Friedman, E. An open letter to the New York Times that was rejected, 2016.

12. Crowther, HA. A confederacy of dunces? Once again, Dixie wants out. The Progressive Populist, 27 (21): December 1, 2021: p. 1.

13. Fang, L, Surgey, N. Lobbyist documents reveal health care industry battle plan against Medicare for All. The Intercept, November 20, 2018.

14. Potter, W. Democrats on the take: New DCCC chair is a best friend of health insurers. Tarbell, March 15, 2019.

15. Evans, M, Herrera, S. Amazon to buy clinic network in bid to expand healthcare. Wall Street Journal, July 22, 2022: A 1.

16. Clemente, F. Billionaires by the numbers. Americans for Tax Fairness & The Institute for Policy Studies Inequality Program, July 15, 2020.

17. Churchill, LR. Rationing Health Care in America: Perceptions and Principles of Justice. Notre Dame, IN: University of Notre Dame, 1987: 103.

18. Sigerist, H. Medical care for all the people. Can J Public Health 35 (7), 258, 1944.

19. Waddill, K. Health insurance consolidation grew from 2014 to 2020. Health Payer Intelligence, September 29, 2021.

20. Shankaran, V. as quoted by Stallings, E. High-deductible health policies linked to delayed diagnosis and treatment. NPR, April 18, 2019.

21. While UnitedHealth reports $24 billion in profits, Americans faced 200 % increases in out-of-pocket costs over last decade. Wendell Potter NOW, January 21, 2022.

22; Geyman, JP. Transformation of U. S. Health Care 1960-2020: One Family Physician’s Journey. Friday Harbor, WA. Copernicus Healthcare, 2022, p. 160.

Friedman, E. The Case for Medicare for All. Medford, MA: Polity Press, 2020, p. 62.