The resurgence of the pandemic further heightened the two-track nature of this recession. Construction and manufacturing, two sectors normally hard hit in downturns, added 51,000 and 38,000 jobs, respectively. Employment in construction now stands 3.0 percent below its pre-pandemic level, while employment in manufacturing is 4.2 percent lower. Finance and insurance added 6,900 jobs in December. Employment is now 0.4 percent above its pre-pandemic level.

By contrast, the loss of 372,000 jobs put restaurant employment 19.9 percent below its February level. The hotel sector lost 23,600 jobs in the month, putting employment 31.8 percent below pre-pandemic levels. Employment in recreation and gambling is down by 30.6 percent, after losing 91,900 jobs in December.

Other big pandemic job losers are air transportation, down 23.4 percent from February; motion pictures, down 42.1 percent; and, sports and performing arts, down 39.3 percent. In December, air transportation added 2,800 jobs, while the motion picture sector lost 3,400 jobs, and the performing arts and sports lost 10,500 jobs.

Retail added 120,500 jobs in December, while health care added 38,800. Employment in these sectors is now down by 2.6 percent and 3.0 percent, respectively, from pre-pandemic levels. State and local government shed another 51,000 jobs in December. Employment in this sector is down by 7.0 percent, almost 1.4 million jobs, from the pre-pandemic level.

One growth area has been couriers, where there has been a rise in employment of 221,800 since February or 26.2 percent. A possible good omen in this report is a rise in temp employment of 67,600. This follows rises of 125,500 and 41,800 in the prior two months, which could mean more permanent hires in the months ahead.

There was little change in the length of the average work week, which stood at 34.7 hours in December. This is 0.4 hours longer than the year-ago level. This means that the reduction in labor demand is being met by laying off workers rather than reducing hours, making the pain from the recession more heavily concentrated among the unemployed.

There also was a rise of 27,000 in the number of long-term (more than 26 weeks) unemployed. They now account for 37.1 percent of all unemployment, far higher than their share in a typical recession. By cause, 28.4 percent report being on temporary layoff, up from 25.9 percent in November. This is consistent with workers being laid off for what are hopefully temporary pandemic conditions.

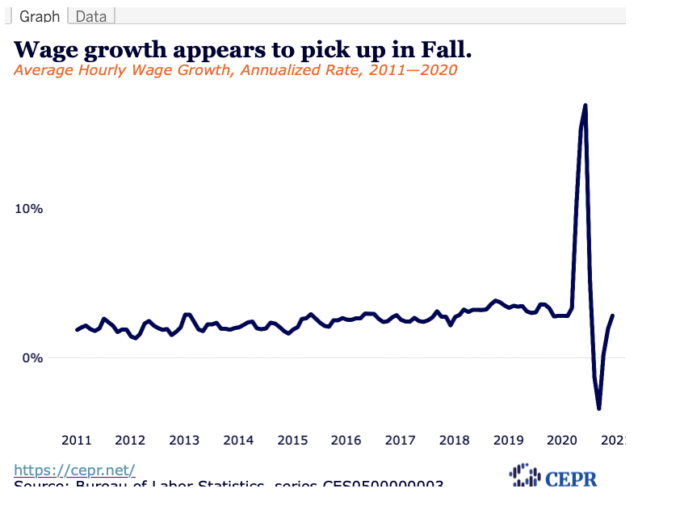

The annualized rate of hourly wage growth comparing the last three months (Oct, Nov, Dec) with the prior three months (July, Aug, Sept) was 2.8 percent. This is somewhat lower than the pre-pandemic pace, but still a healthy pace. We saw very strong productivity growth of 4.0 percent reported for the year ending in the third quarter of 2020. If anything close to that pace is sustained it should allow for more rapid wage growth going forward, although we will likely need a much tighter labor market to see it.

Most data in the household survey did not show large changes. An exception is a sharp rise in Hispanic unemployment, which rose from 8.4 percent to 9.3 percent. These data are erratic, but this rise would be consistent with the loss of jobs in restaurants and hotels. On the other side, there was a drop of 0.8 percentage points in the unemployment rate of Asian Americans to 5.9 percent, although this was entirely due to people leaving the labor force, as their employment rate actually dropped slightly.

This is a very mixed report in that the labor market is definitely being hard hit by the resurgence of the pandemic. On the other hand, the continued strong growth in sectors like construction and manufacturing bodes well for the economy once the pandemic is under control, as does the respectable pace of wage growth we are now seeing. If we can sustain the unemployed through the period where the pandemic continues to be widespread, we can expect a bright future later in the year.

This column first appeared on Dean Baker’s Beat the Press blog.