A Weekend at Bernie’s

The current election ‘cycle’ in the U.S. is being met with what is increasingly argued to be changed circumstances. The rise of ‘outsiders’ Donald Trump and Bernie Sanders plays into the storyline of an atrophied political mainstream in need of an infusion of fresh blood to challenge ideas that aren’t working for most people. Was the problem simply a matter of stale ideas rather than the institutions and the whole of the Western corporate-state dedicated to the ongoing consolidation of political and economic power in the hands of a small and remote plutocracy the ‘inside / outside’ dichotomy might be more functionally descriptive. And as the ever-troublesome facts have it, both Messrs. Trump and Sanders have spent their adult lives in the corridors of power, albeit in different spheres.

Mr. Trump is an inheritance baby who used his economic power to turn New York from an artistically inclined metropolis into a banker ghetto where ever-increasing expanses of the city serve as empty ‘luxury’ bank accounts for an international lootocracy. Bernie Sanders has spent the last twenty-five years posing as an outsider in Washington while acting as a functionary for the U.S. imperial project. For reasons outlined below Mr. Sanders’ proposed economic ‘reforms’ constitute the same capitulation-in-waiting with which he launched his campaign by promising to bow-out gracefully when Hillary Clinton finally receives the nod from the Democrat establishment. The great mystery of the political moment is whether the status quo will cease to exist in spite of Messrs. Trump and Sanders, not because of them.

Graph (1) above: the U.S. / multinational corporate response to global monetary policies has by-and-large been what Central Bankers were hoping for, but for all of the wrong reasons. Since 2008 corporations have borrowed large amounts of money, but rather than using the proceeds to invest in ‘their’ businesses they have repurchased stock to raise the value of the stock options that executives and compliant Boards of Directors have granted themselves. The political relevance is that the resulting excessive private debt is destined to produce bad outcomes. How far would Bernie Sanders get with ‘insider’ reforms in the midst of another global economic meltdown? Without a revolutionary program those who control the economy control U.S. politics. Data source: SIFMA; Original image source: fineartamerica.com.

Left largely out of public consideration to date is that over the last four or so decades the economic policies that have been enacted had a constituency amongst the powers-that-be. From deregulation begun in the 1970s to financialization, faux fiscal probity in the service of banker interests, bailouts and neo-imperial trade agreements, apparent ideological confusion is better explained as policies designed to consolidate economic power. The practical relevance is that should Mr. Trump find his way to the White House his punishing misreading of (Paul) Volcker-nomics would find a receptive audience amongst self-interested bankers. Should Mr. Sanders find his way to warming a chair as President ‘profitable’ foreign entanglements that are his forte in capitulation would be the product of choice amongst establishment predators.

Providing a veneer of pragmatism to predatory public policies has been the distance between ‘the economy’ as it exists and the rank ideology put forward as economics by economists, politicians and self-interested business persons. Through historical particularity the only fiscal constraints that the U.S. has at present are political and bi-partisan. The relation that tax receipts bear to government expenditures is as accounting entries, not as functional constraints. Poverty, unemployment and food and housing insecurity are gratuitous from the perspective of social capacity. Additionally, the rich are rich in large measure through government transfers, subsidies, protections, asymmetrical property ‘rights’ and standing armies as both economic sop to connected insiders and the muscle behind imperial predations. Economic constraints do exist, but conventional explanations of them are self-serving nonsense.

On the flip side of fiscal mythology are center-left monetary fantasies that leave Keynes’ useful insights behind to support the worst that finance capitalism has to offer. As with the consolidation of market power by large corporations, finance capitalism has ‘inside’ and ‘outside’ uses and prices for financial capital that bear no resemblance to the ‘market’ relations of mainstream theory. Asset-stripping, labor outsourcing and economic instability attributable to finance-run-amok from cheap financing have put more people out of work than low interest rates could ever reverse. Financing costs are marginal to all but highly leveraged, largely financial, corporations and the mainstream models that suggest otherwise misrepresent bank money creation even more egregiously than fiscal ‘hawks’ misrepresent national accounts.

How We Got Here

When Bill Clinton entered office as President in 1993 he appointed former Goldman Sachs executive Robert Rubin to lead his National Economic Council. Almost immediately Mr. Rubin ‘informed’ Mr. Clinton that the Federal budget deficit was larger than anticipated and that government expenditures, starting with Mr. Clinton’s promised increases in social spending to offset the residual of recession, would have to be cut to balance the budget. In truth, as Mr. Rubin and the rest of Mr. Clinton’s economic advisors either knew and misrepresented or didn’t know, the budget deficit presented no factual hindrance to increased social spending. Government expenditures are but accounting entries credited to the accounts of vendors— the only limit on social spending that Mr. Clinton faced was self-imposed under the lie that it was the result of a budget constraint.

Eight years after Mr. Clinton left office, in the midst of the worst economic crisis since the Great Depression, Democrat President Barack Obama again raised the specter of budget deficits to limit social spending while simultaneously creating ‘out of thin air’ tens of trillions of dollars in transfers, guarantees and loans to ‘save’ Wall Street from its prior decades of predatory and socially destructive business practices. The juxtaposition of unlimited bailouts for bankers with gratuitously limited funds for their victims who lost their jobs, houses and life savings is one of the political miracles of the modern age— America’s ‘first Black President’ knowingly consigned a significant proportion of his nominal constituency, in particular American Blacks, to perpetual poverty for the benefit of bankers who by-and-large should have gone to prison for their crimes.

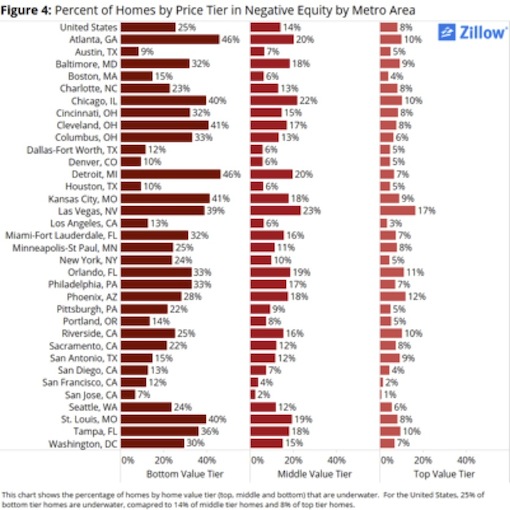

Chart (1): illustrates the ‘tiered’ residual in 2015 of the housing boom-bust engineered by bankers and covered up by Barack Obama and his administration. Houses in the lowest price group (tier) remain catastrophically underwater— worth less than the amounts owed against them, followed by those in the middle and finally, the top tier. The specific targeting of poor neighborhoods, particularly neighborhoods of color, by predatory bankers relied on a history of economic dispossession to make loans that stood little chance of being repaid. The practice inflated housing prices assuring that most of the loans made were for amounts greater than the houses were worth to make bankers rich through bonuses paid before the loans soured. The bailouts restored culpable bankers while the underwater ‘bottom value’ tier catalogs the social destruction left behind. Source: zillow.com.

A question worth asking is why the nominal political leadership and the near totality of the economics ‘profession’ misrepresent the relatively straightforward process of government spending? An attendant mystery is why the economics mainstream, including liberal and progressive economists, continues to push the ‘loanable’ funds model of bank lending when even Central Bankers argue that it is misleading nonsense? The points of relevance are that poverty, unemployment and economic dispossession are the flip side of equally socially determined government spending that makes and keeps the rich wealthy. In the absence of binding budget constraints poverty and unemployment are policy choices. And without the loanable funds model banks and bankers are on the hook for poorly made loans, not depositors.

When this understanding is applied to the actual policies of Messrs. Clinton and Obama what becomes apparent is that they have been very effective class warriors on the side of oligarchy. Economists working from fraudulent monetary models and Washington Consensus economics support these convenient fictions pushed by the financial classes to benefit themselves. The Washington Consensus is creditor (banker) economics put forward as the economic facts of nature. Limiting ‘inflation,’ the oft implied rationale for the fiction of binding Federal budget constraints, is carefully delineated to exclude banker-friendly asset price inflation. And defining ‘the economy’ at the level of ‘system’ nets fat banker paychecks against the social carnage they cause to claim a social benefit from mass economic destruction.

‘Washington Consensus Policies’

* Fiscal discipline

* A redirection of public expenditure priorities toward fields offering both high economic returns and the potential to improve income distribution, such as primary health care, primary education, and infrastructure

* Tax reform (to lower marginal rates and broaden the tax base)

* Interest rate liberalization

* A competitive exchange rate

* Trade liberalization

* Liberalization of inflows of foreign direct investment

* Privatization

* Deregulation (to abolish barriers to entry and exit)

* Secure property rights

Conversely, from where did tens of trillions of dollars suddenly appear when Wall Street was on the precipice? In terms of crude relevance, how gullible must a people be to believe upper-class claims that the lower classes are ‘takers’ when the upper classes have all that there is to be taken in their own pockets? Were it not for the political content of such claims one might think the rich would better serve their own interests by shutting their mouths. But the divide and conquer strategy in use is effective— middle-class blowhards who see their five shares of stock rising with the fortunes of the rich see a similarity of interests that is distinctly not reciprocated. As wage growth has atrophied, employment becomes ever more tenuous and tenuously supportive and promised benefits become less probable, the economic class that has the ear of the political class see all but themselves as ‘takers.’

The level of misdirection at work isn’t possible without a helping hand from dominant, and wholly misleading, economic mythologies. If binding budget constraints were fact Wall Street would have been resolved instead of bailed out in 2008. Economic dislocations would have resulted, but tell that to the citizens of Baltimore and Detroit who were preyed upon by malevolent bankers and now live in poverty and violence with the results. And if clever-lite bankers destroyed their own businesses but retail customer deposits weren’t at risk (because of Federal deposit insurance), why should working people have been called upon to care? In fact, U.S. Bankers got paid twice to destroy America’s cities— the first time through bonuses for making and securitizing predatory loans and the second time through bailouts.

Graph (2) above: had Barack Obama wanted to increase government spending to fund a government jobs program and / or to provide housing and food security for the people whose lives were destroyed by the economic calamity caused by Wall Street he had both historical precedence for government spending in the public interest and all of the funds he needed to do so available to him. Only a few years earlier the (George W) Bush administration had effectively sold and funded resource-wasting vanity wars while passing tax cuts that overwhelmingly benefitted the very wealthy. Apologists claim that Mr. Obama was constrained by Congressional Republicans while the facts have it that he is ideologically beholden to Washington Consensus economics while favoring his financial contributors from Wall Street. Source: St. Louis Federal Reserve.

This story goes in two directions from here: the economic policies deemed politically feasible derive from the bogus premises of those doing the deeming and the ‘unintended’ consequences of past and present policies are wholly intended once the premises are seen as bogus. Ironically for Democrats, it was none other than Republican devil Dick Cheney who made the point that “deficits don’t matter” meaning that the (George W.) Bush administration was free to squander public resources on whatever poorly considered wars of choice it could conceive. Mr. Bush even promoted the Keynesian economic project soon to be summarily rejected by Democrat Barack Obama except inasmuch as corrupt, incompetent capitalists were bailed out for torpedoing their own businesses along with the global economy. Government spending grew less under Mr. Obama than any other President since Herbert Hoover.

Graph (3) above: the flip side of foregone fiscal policies is monetary policies designed to benefit financial speculators, a/k/a Wall Street, at the expense of the ‘real’ economy on which the rest of us depend. The oft made contention that the Federal Reserve only controls short-term interest rates was put to the test through QE (Quantitative Easing) designed to lower longer-term rates. Illustrated is the muted decline in corporate borrowing costs represented by BAA yields versus the sustained period of 3-month LIBOR, a widely used financial borrowing rate, near zero. The clear goal of Western Central Banks was to reflate the value of financial assets by providing copious quantities of cheap leverage. Corporations wouldn’t be induced to fund new economic activity by a 1% – 2% decline in corporate borrowing costs except inasmuch as corporate executives could borrow on the corporate dime to raise the value of the stock options they were / are granting themselves. Source: St. Louis Federal Reserve.

Under the guise of fiscal probity Democrats Bill Clinton and Barack Obama both claimed that budget deficits prevented them from increasing social spending. Mr. Clinton cut ‘welfare as we know it’ as a sop to nascent class warriors motivated by Ronald Reagan’s racist attack on the poor. Once it is understood that the fiscal constraints Mr. Clinton faced were wholly contrived what becomes apparent is that he could have put the theory of ‘moral hazard,’ that ‘poor people are poor because they are lazy,’ to the test with a Federal program of guaranteed employment at a living wage plus benefits. Barack Obama claimed the same faux fiscal constraint to explain his aversion to social spending even as he bailed out Wall Street with tens of trillions of dollars in public resources. To those who argue that Mr. Obama’s ACA (Affordable Care Act) is social spending, the stock prices of health insurers suggest that Wall Street sees it as what it is— a corporate giveaway.

The Graveyard of Social Movements

Even if Bernie Sanders is sincere with his populist economic proposals, the Democrat Party is the wrong vehicle for getting them implemented. The saying “the Democratic Party is the graveyard of social movements” exists for a reason. Mr. Sanders’ history-to-date is of taking principled stands prior to capitulating to political pragmatics as seen through the lens of the two-Party political patronage system. If one buys the Democrat apologetics for Mr. Obama’s policies, that they were ‘the best that he could do under the circumstances,’ it is the circumstances that need changing, not the cast of characters. If one grants both agency and continuity to the policies of Democrats Clinton and Obama, they are simply better salespeople for an empire turned inward against the poor, vulnerable and what remains of the middle class.

The related argument that if one wants to have a political impact it must be within the two-Party system meets the question back of precisely what type of impact it is that one wishes to have? While I’m delighted that a Black person was elected President of the U.S., Barack Obama’s actual policies have filled the traditional Democrat role of restoration of empire— recall that Bill Clinton’s posture of fiscal responsibility was a lie used to sell a vicious and punitive class war against the poor and vulnerable. Mr. Obama’s restoration of Wall Street rebuilt the mechanisms of economic extraction for a self-interested oligarchy. National maps of Wall Street’s predatory lending in the housing boom – bust overlap almost perfectly with the recent growth in extreme poverty and violence.

The Americanism that compromise is a virtue ties to a Platonic misreading of the Aristotelian ‘centeredness’ of his ‘Golden Mean’ as the locus of truth. This same idea drives the ‘spectrum’ view of political / economic ideology that places left and right as extremes of a singular view rather than as oppositional, and therefore irreconcilable, views. Economists and the economically inclined can see this difference at work in mainstream efforts to cram Marx’s labor theory of value into a neoclassical frame. MIT technologist and uncle of demon spawn Larry Summers, Paul Samuelson, dismissed Marx as a ‘minor Ricardian’ because he only knew / understood Marx’s theory through a Platonic frame meaning that he didn’t understand it at all. While this is far more than most readers likely wanted to know, the relevance is that the American view of compromise is in significant ways a restatement of the base premise of capitalism as a ‘self-legitimating’ system— in the ‘correct’ circumstances market outcomes are the embodiment of an externalized ‘truth’ of nature, God, or whatever, much as compromise. Without this externalized ‘truth’ market outcomes are the result of social struggle and any unity of interests through economic ‘system’ disappears.

In contrast, all of the major Party candidates are ‘spectrum’ politicians meaning that their frames of reference take the existing order as given. The related incrementalist view that some is better than none, that a shift this way or that is better than no shift at all, draws a circle around local achievements to the exclusion of both the larger outcomes to which they contribute and the realm of social possibility. Within the frame of ‘compromise,’ Mr. Obama’s bailouts of Wall Street would have been a compromise if Wall Street had been shut down, a few thousand bankers had gone to prison for their crimes and the rest lived out their lives as modestly paid functionaries in newly created public banking utilities. Another compromise would be only hanging the top Bush administration officials responsible for the War in Iraq instead of the whole lot. As is stands, compromise is apparently a euphemism for surrender.