Greece

In terms both gratuitous and sadly predictable, last week’s ‘no’ vote in Greece was followed by insistence from the Troika, led by German Chancellor Angela Merkel, that the Greek government accept economic ‘reforms’ likely to be even more onerous than those that preceded the vote or face a quick exit from the European Monetary Union (Grexit). With long precedence of capitulation to Troika demands by center-left Social Democrat governments across Europe, now apparently joining this macabre dance is Greek Prime Minister Alexis Tsipris who, only days after winning consent from the Greek people to take on the Troika, is said to be offering more austerity in exchange for ‘face-saving’ cuts in unpayable levels of debt.

Earlier reports attributed to Greece’s recently replaced Finance Minister Yanis Varoufakis had it that the Syriza leadership had believed that last week’s referendum would never pass and had planned with a ‘yes’ vote to resign and let a new government accept the Troika’s terms. However, the badly played hand simply reaffirmed what was already apparent: the Troika, in particular the Germans, has no regrets for the failed economic policies it has inflicted on the Greek people and sees blind submission to even more failed economic policies as the only response it will accept. Given this history, the choice that Syriza faced was / is between a quick and disorderly exit from the Euro and capitulation that will most likely force an eventual exit with even fewer resources.

Picture: No Exit by the Troika. Limited engagement with the current cast: Angela Merkel, Alexis Tsipris and Wolfgang Schaeuble— hell with all of the austerity and no place to hide. Original image source: corvallistoday.com

The absence of a good choice placed the onus on Greek Prime Minister Alexis Tsipras to make the best of a bad situation that was in fact compromised from the moment Syriza took office. The mandate to both renegotiate the Troika’s austerity policies and remain within the monetary union only made sense by assuming the Troika was interested in constructive outcomes when it had already established that it wasn’t. Now, having ‘won’ the referendum, capitulation tosses democratic accountability into the garbage heap in exchange for short-term political resolution. The European Monetary Union is unworkable in its present incarnation. And as Germany has demonstrated, there is no political will to make it workable through further fiscal and political integration. An exit now would make Greece but the first to go in the eventual dissolution of the union.

With history as a guide, the problem with forcing repayment of unrepayable debts is that they are unrepayable. As the saying goes, you can’t squeeze blood from a stone. Concessions on reducing levels of debt may provide short-term political cover from those who aren’t paying attention. But acceptance of more austerity means that the debts would have become even more unrepayable anyhow. The way to repay debt is to grow the capacity to do so, the opposite of what the Troika is demanding and that Mr. Tsipris is said to be offering. This capacity is a matter of simple arithmetic, not complicated theory. And the last five years of austerity policies have resulted in increased debt with diminished capacity to pay— the opposite of what the Troika predicted when the policies were enacted.

Picture: The good citizens of Argentina express respectful disagreement with the austerity policies of the IMF and the predations of international bankers. The citizens of Greece have expressed similar disagreement in the past. Original image source: libertadyprogresonline.com.

Greece and Argentina

The case of Argentina’s exit from a U.S. dollar peg in 2001 is being put forward as a possible model for a Greek exit from the Euro without discussion of the damning history that ties both to the American and European neoliberal ‘projects’ and without the particulars that could make the Greek case more disruptive. Argentina in the 1990s was a neoliberal laboratory where a ‘radical left’ that was voted into power to counter neoliberal policies almost immediately began implementing the agenda of international capital complete with handing the Argentine economy over to international bankers, industrial scale corruption and the privatization of Argentine state assets for pennies on the dollar for the benefit of foreign capitalists. Bank deposits were seized to make foreign speculators whole and crucial infrastructure like the distribution of water was privatized to squeeze peasants for every penny that could be taken.

This history ties to the case of Greece in a number of dimensions. The growth of the European Monetary Union was coincident with the rise of neoliberalism across Europe. The austerity economics being implemented in the European periphery is straight neoliberal dogma— the IMF has been using austerity against ‘debtor’ countries for the last half-century. This doesn’t mean there aren’t racial and nationalist contributors to the European North’s treatment of the South in the present, just that it also finds less politically incendiary explanation in punishing economic policies. Likewise, ‘internal’ Greek plutocrats were used as agents of international capital, corruption was rampant, private debts were placed on the public balance sheet and pensions have been raided for the benefit of European bankers and hedge funds.

Nothing I’ve read suggests that Syriza is corrupt per se. And a question for current critics is: what will be the likely outcome of Greek capitulation to Troika demands once austerity and the privatization of Greek assets have left nothing to take and Greece is still forced into a disorderly exit from the monetary union? If the premises are that the Troika is pushing an economics of gradual dissolution and the monetary union is fatally flawed without fiscal and political integration that no one at present is seriously considering, from where do good outcomes emerge? Any move by Greece toward independence, as would be the case with the long preparation needed for an orderly exit from the monetary union, has already been flagged by the Troika as a move against creditors.

A central difference between Argentina and Greece is that ‘all’ that Argentina had to do was to break the peg (fixed currency exchange ratio) with the USD while implementation of the Euro was a massive technological undertaking that replaced the Greek technology and institutions that supported the drachma. In the event of a forced Greek exit recovery of these technologies and institutions would take time that the Greeks don’t have. Breakdown of the supply-chain— the integrated economic relations that together facilitate economic production, causes a cascade effect where once lost, has to be rebuilt from the ground up. In the case of a forced exit the Troika should be held to account for disruptions to the Greek economy. But the question of who would force them to act in Greece’s favor has no immediate answer.

In political terms, given that 61% of Greeks just voted to tell the Troika where to stick their austerity, Mr. Tsipras’ acceptance of more of the same is a political disaster that is certain to be accompanied by increased economic suffering. No matter that there were no real economic alternatives left open, the misdirection of holding the referendum when the intention was to hand the chore of capitulation over to a new government leaves the political landscape open to the radical right. The leader of the French National Front, Marine Le Pen, publicly lauded the Greek ‘no’ votes creating an opening for those saying they will take the Troika on, including Greek neo-Nazis in the form of Golden Dawn. In history, a promise to end economic chaos completed the ideological circle from corporatism to radical nationalism and brought the Nazis to power in Germany in the early-mid twentieth century.

When Neoliberalism Met Finance

The only real ‘alternative’ for Greece appears to be the timing of increased catastrophe, either now with its attendant political disruptions or later in what will most probably be diminished circumstances. In broader historical terms, the very same neoliberal program that crushed Argentina in the early 2000s is crushing Greece in the present. (The argument that the currency peg is to blame in Argentina is absurdly reductive— two decades of neoliberal setup preceded full blown crisis). The larger picture is international, is decades in the making and is being moved forward without interruption or regret through ‘trade’ deals being pushed by Western liberals, through the increasing privatization and diminishment of the public sphere and through the police, the courts and the technologies of social repression.

The irony of U.S. President Barack Obama lecturing the Greek leadership on compromise and the importance of political continuity is that Mr. Obama’s economic policies have been virtually indistinguishable from those of the European North. Had it not been for the political incompetence of leading Republicans Federal public pensions (Social Security) would have been cut to ‘balance the budget’ (SS has a separate budget). Federal ‘mortgage relief’ programs (‘bailouts’) were cynically conceived to ‘foam the runway’ with the lives and life savings of ordinary citizens. The Affordable Care Act (Obamacare) is the ‘market-based solution’ that its supporters deserve but that its victims will receive. And austerity chatter, as well as policies, was just as loud, insistent and uninformed in the White House as it was in the darkest recesses of Troika meeting rooms. Between flat Federal expenditures and declining state expenditures, austerity was the official U.S. response to recession for the first time since the Great Depression.

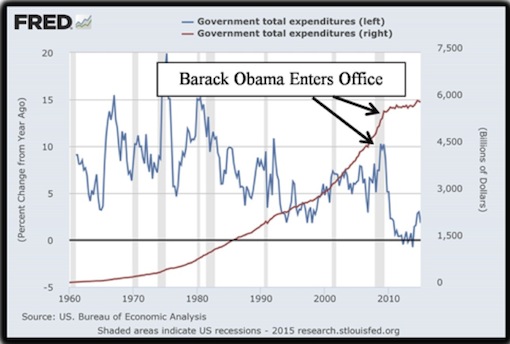

Graph (1): Revisionist history from Europe and Democrat apologists in the U.S. places U.S. President Barack Obama’s economic policies as direct descendants of FDR’s New Deal when they more accurately reflected the class warfare of Wall Street’s finance-based neo-liberalism. Government spending saw the lowest growth in modern history after crisis hit in 2008. The much lauded rise in the debt to GDP ratio is for those who slept through arithmetic class. If the denominator (GDP) declines while debt levels remain stable the ratio rises. Mr. Obama’s ‘stimulus’ was mostly tax cuts and ‘incentives’ when fiscal policies could have given every American who wants one a job at a living wage. Source: St. Louis Federal Reserve.

For the historically inclined, Charles Kindleberger’s The World in Depression offers a liberal explanation of the Western back-and-forth over national debts from WWI that contributed to the persistence of the Great Depression and to the conclusion of WWI with WWII. The IMF (International Monetary Fund) was created by the U.S. following WWII to ‘manage’ national accounts with the U.S. acting as benevolent hegemon. Austerity economics tie to pre-Keynesian national accounts machinations, the basic framework of which became standard IMF policy. The position of benevolent hegemon placed the U.S., with its historical beginnings in slavery and genocide against the indigenous population, as a liberal institution with international interests. Actual history ties current German policies against the European periphery to U.S. ‘paternalism’ that served imperial capitalism under a guise of benevolent internationalism.

There came a surreal moment around 2011 when Wall Street analysis—analysis, not policy recommendations, went far to the left of the liberal and progressive political mainstream in the U.S. to argue that Western government policies to support bankers and industrialists against the broader public interest demonstrated the supporting role that governments play in capitalist economies that Marx had identified. Many on Wall Street had assumed that 2008 was the end of business-as-usual for generations to come when the neoliberally-disposed President Obama ‘pleasantly surprised them’ with his policies. The center-periphery political geography (imperialism) now so evident in Europe was largely left out of the analysis. But of interest is the theoretical rupture that moved it from the incrementalist ‘spectrum’ view under which Western leaders shift policies incrementally left or right to one of a struggle between opposing class interests.

As Wall Street was recovered through monetary policies its analysis reverted to its self-serving makers / takers theory of divine distribution. Also recovered was Wall Street’s (large American, German and French banks) capacity for uncreative— thuggish, brutal and self-interested, destruction. Pirate capitalism soon had prominent hedge fund managers placing ‘bets’ that the European periphery, in particular Greece, would fail. Behind the bets was the capacity to use Western governments to create self-fulfilling outcomes— the 2010 ‘rescue’ of Greece, in which unpayable debts were coupled with austerity economics, was to pay off the hedge funds and large banks that had brought Greece to the edge of collapse. The ‘analysis’ used by predatory financiers came straight from the IMF’s national accounts policies. Incredibly (not), economic austerity for the benefit of creditors was their recommendation.

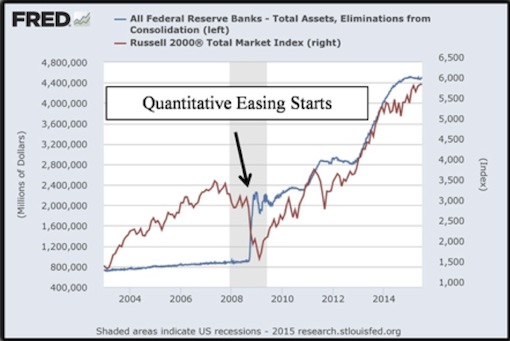

Graph (2): With apologies for trotting this old standard out yet again, it has current relevance. By 2009 the Federal Reserve, the central bank of the U.S., began implementing aggressive monetary policies to revive asset prices. Illustrated here is the relationship between Quantitative Easing, the Federal Reserve’s program of purchasing longer dated assets, and stock prices. Fiscal policies like a government jobs program to provide employment for the unemployed at a living wage are more direct and more effective in restoring the broad economy. That monetary policies that benefit the rich were quickly and robustly undertaken while fiscal policies were small and purposely ineffectual (half monetary) is a central reason why Wall Street claimed that Marx’s analysis of capitalism was correct before ‘recovery’ fully kicked in. Source: St. Louis Federal Reserve.

Revisionist history now being put forward in the U.S. and Europe has the U.S. since 2008 pursuing liberal policies while Europe tightened the screws. The ability of U.S., British and Japanese governments to create unlimited amounts of money was / is the central institutional difference between these and Europe, but otherwise austerity economics— limitations placed on social spending under the contrived illusion / delusion that tax receipts place a limit on government spending, were wholly endorsed by the American and European government leaderships alike. U.S. President Obama argued early and enthusiastically that the U.S. faced the same fiscal limitations as Europe with the effect that economic policies were handed to central bankers to determine. Of interest was that these theorized limitations were met by unlimited resources made available to bankers who had killed their businesses.

One of the conceptual wins of capitalism and capitalist economics is the idea that economic growth represents the normal working of capitalism and that recessions are an aberration. Political chatter becomes about how well this or that politician responded to recession and not about what arrangement of circumstance caused it. When U.S. President Barack Obama entered office he ‘inherited’ ‘difficult circumstances.’ When German Chancellor Angela Merkel forces ‘expansionary austerity’ on the European periphery it is to restore economies to their ‘normal’ working. Austerity might be bitter medicine, but it is given to bring the system of the economy back to its normal working order, goes the reasoning.

In political terms, if recession is as normal a part of capitalist economies as good economic times the circle draws tighter— restoration of the good times is also restoration of the bad times. And defense of this system that so regularly produces both good and bad times assumes some degree of distributional neutrality, that good and bad are shared by type, if not precisely by degree. Beginning in the mid-1970s, but in particular since the onset of the Great Recession, the wealthy, in terms of both class and imperial geography, have pushed government policies that benefit themselves by taking from the rest of us. ‘Expansionary austerity’ has been used across the West to cut or limit social spending under the premise / promise that economic growth will make up the difference.

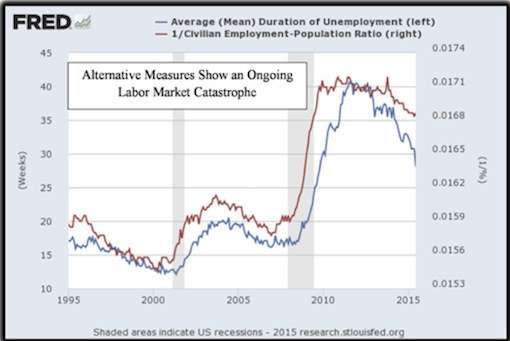

Graph (3): The dominant economic narrative in the U.S. is of economic recovery when there is evidence that the residual of the Great Recession is deep and ongoing. The mainstream explanation of the fall in the proportion of the working age population that is employed (above, inverted) is that ten million people retired within a few weeks of each other in 2008. Left out of this explanation is that the average tenure of unemployment follows this decline in employment, with both remaining at levels that signal economic catastrophe for the American periphery. Other indicators do signal recovery and the intent here isn’t to ‘trash-talk’ the economy. What these indicators suggest is that for parts of the economy, the American ‘periphery,’ the American experience is tied more closely to that of the European periphery than to the Western ‘center.’ Source: St. Louis Federal Reserve.

One impact that capitalist growth and recession cycles have is that economic decisions like taking on debt that may make sense during a growth phase become untenable during the recession phase. A saying is that people, companies and nations get into more trouble in good times than in bad. The framing of recessions as unexpected accidents puts a moralistic chide atop a normal aspect of capitalism that is made worse by the existence of for-profit banks. Peripheral Europe didn’t become untenable because of debt levels until after Wall Street killed the global economy in the run-up to 2008. Wall Street created the circumstances that both the European North and the U.S. have used to further a fundamentally imperialist stance toward ‘borrowers’ who are also both citizens and customers. The ideological sleight-of-hand that recessions are unexpected requires setting aside the history of Western capitalism.

An associated misdirection is the contention that the U.S. economy has recovered from crisis since 2008 inferring moral / structural / institutional impurities where ongoing dislocations are less well covered over. The remainder of the European periphery trails only slightly behind Greece in levels of conspicuous economic misery. And amazingly, the same Great Depression economics that had 25% of the industrial U.S. workforce quitting their jobs to go on vacation in 1932 today has ten million workers ‘retiring’ in a matter of weeks of each other coincident with the worst of recessionary layoffs in 2008. There is no dispute that there are nuances to measuring economic performance. But if employment always declines in recessions (it does) and employment fell off of the proverbial cliff in 2008 and by the same measures has remained there since, how plausible is the storyline of recovery? Put differently, what is recovery if actual human beings don’t benefit from it?

The circumstance of Greece today is an economic and moral catastrophe, but it is an engineered catastrophe. In the half-century that the IMF was implementing austerity economics before the creation of the European Monetary Union there was never the pretense that austerity was intended to benefit indebted nations. Austerity is gangster economics intended to pay off creditors no matter how destructive the consequences were / are to the masses of people who are forced to suffer it but that had no part in incurring the debt and saw no benefit from it. As seamless as the neoliberal project at times appears, it is always within a short distance of joining radical nationalism through conflation of poorly engineered economic interests with joint political interests. The German view toward the European periphery now borders on rigid nationalism in the context of unreflective adherence to radical capitalist ideology. And the neoliberal project is proceeding apace in the U.S. Absent an enthusiastic revival of left political economy, the future appears grim.