There have been efforts to rewrite the history of the economic and financial crises of recent experience since the days they first became evident in 2007. Two main tacks have been taken: the first is to place the genesis of the crises in nature as unfortunate accidents and the second is to minimize the damage done, the lives ruined, to claim that all is now well. Whether or not things have improved depends very much on one’s place in the economic order. The tiny fraction of the populace that ‘owns’ most of the wealth is doing quite well whereas peripheral Europe and the peripheral U.S., not so well. To the punchline: the excessive private debt that sank the global economy in 2008 remains unresolved while the powers that be have convinced most people that public (government) debt is the problem.

This is to grant that there is long history of using crisis hyperbole to sell ideas, usually bad ones. But the facts of recent decades, the rolling crises tied to banking and finance, have shared genesis in excessive private debt, in arbitrary limits on public debt and in conflation of public with private debt to create both false dilemmas and future crises. Western politicians may be ignorant of the specifics, of the scale and mechanics of economic catastrophe generation, but bailout dependent bankers have no such excuse. No crystal ball is needed to relate the genesis of past crises to present circumstance. Financial ‘deepening,’ embedding finance deeper and wider into an interdependent global economy, has continued apace since 2008 and the forces that sank the global economy then are larger and more deeply embedded now than they were before the last crisis.

Graph (1) above: debt is a draw against future economic production. The greater the (private) debt in relation to this production the more crisis prone economies can be. In recent decades Wall Street, including large European banks, has massively expanded the quantity of credit (financing) relative to economic production in Western economies. This has resulted in the deterioration of lending standards explained alternately as banks competing for borrowers (Minsky) or as organized looting. This characteristic of credit expansion, of making loans to decreasingly credit-worthy borrowers, is in large measure what makes high private debt levels so dangerous. With recent history as a guide, bailouts of Wall Street without prosecutions for widespread criminal behavior create and perpetuate kleptocracy. Units are percentages. Source: World Bank.

When U.S. President Barack Obama conflated government debt with household debt he did more than make a false analogy. The Federal government in the U.S. can legally create money while households that do so go the prison if they are caught. Left unaccounted for is this financial deepening process, the increased reach that finds credit inserted into ever more tenuous parts of Western economies. In each of the last three economic downturns, the S&L crisis of the late 1980s – early 1990s, the dot-com bust of the early 2000s and the housing bust of 2006 – today, a larger percentage of wholly implausible ‘businesses’ were kept alive through new loans to replace old loans, not through producing something that people want. Wall Street itself is a prime example of this tendency— risky ‘bets’ and interdependencies would have ended it in 2008 had market forces run their course.

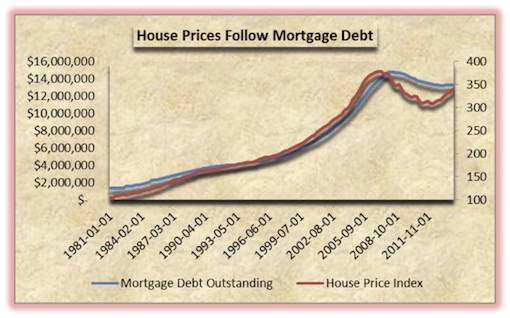

Graph (2) above: the credit quality deterioration that is part of the credit expansion process remains a mystery to the economic mainstream because it requires integrating the interests of banks and government. In the early 2000s the (George W) Bush administration began actively lowering mortgage lending standards, in part by having his administration issue lax national standards that superseded more rigorous local standards. The same happened in Europe with no help from Mr. Bush illustrating the systemic nature of the tendency. The process is often explained as ‘underpricing’ risk. But had credit standards been maintained many of the loans that accumulated to crisis would never have been made and the global property bubble would have been averted. Graph (2) illustrates the relationship of mortgage debt to house prices. The drop in mortgage debt outstanding is from bank write-offs of uncollectible debts and eight years of payments made against the mortgages since crisis emerged. Units are millions of dollars (left scale) and House Price Index (right scale). Source: St. Louis Fed.

Here two related premises are often brought to bear— (1), ‘we’ need a functioning credit system and (2), the effects of the last crisis are receding pointing to their temporary nature. The lingering Depression in Europe is as much a product of this credit expansion process as the mortgage bust in the U.S. was / is. Credit that should never have been extended led to property bubbles across Ireland, Spain, Portugal and Greece as well as major American cities and regions. The mainstream economists’ explanation of ‘excess savings’ renders harmless the Wall Street lootocracy that knew it was making improbable loans to people who couldn’t afford to pay them back. Both the neo-classical and better informed heterodox ‘national accounts’ schools support the radical center against the observation that the rich used Wall Street to make themselves richer while screwing the rest of us. Class warfare anyone? Anyone?

Graph (3) above: the flat line across the bottom of the graph is the Average Real Wealth per Family for the ‘bottom’ 90% of the U.S. population. The red line represents that of the top 0.01%. And in fact, since the start of ‘recovery’ the incomes and wealth of the very richest have largely recovered while those of the bottom 90% have remained about where they were in 2009. The ‘centrist’ policies that brought about these outcomes can be seen as ‘fringe’ when one considers that a tiny fraction of the population has benefited while the vast majority hasn’t. Source: Emmanuel Saez.

Poor policy choices and the base frame of the Maastricht Treaty and related institutional constraints have made the Depression in peripheral Europe worse than in the U.S. But the center – periphery frame of earlier ‘agreements’ like Bretton Woods overlaid with the distribution of Wall Street power would place economic misery about where it has fallen as well. This can be seen inside the U.S. with the impact of crisis distributed along the class, race and gender lines that preceded it. Greeks worked longer hours for half the pay of Northern Europeans before crisis struck. Power imbalances have been reconstituted through these ‘passive’ institutional arrangements to keep those on top there. Western corporations and Wall Street understand this strategy well.

The argument back, that economic relations needn’t be zero sum affairs, is left to explain the history of Western capitalism. Put differently, wouldn’t all of Europe (and the U.S. for that matter) benefit from economic growth that austerity policies preclude? Austerity policies are banker economics. Wall Street created sequential crises of increasing scope and scale and then used its political power to set austerity as public policy. And since nominal ‘recovery’ began its beneficiaries can be placed quite comfortably in the frame of the class interests served. So, to the point made regularly in recent years: Keynesian policies, particularly fiscal policies, make more sense than banker economics. But these clearly aren’t the policies being implemented. To view this as an accident requires overlooking the existing distribution of economic power.

This point is being made, perhaps to the level of overkill; because it is the political and economic ‘center’ that is fringe in the sense of representing the interests of a tiny portion of the populace against those of most people on the planet. Democrat Barack Obama supports trade agreements that undermine labor and environmental regulations while claiming the centrist position that a ‘balance’ of interests is his goal. Mr. Obama dedicated his administration to reviving Wall Street and keeping its malefactors out of prison with the result that over 90% of the ‘recovery’ has gone to the richest one percent of the population. And the Social Democrat Parties of Europe have been neo-liberal sell-outs for some decades now. The ‘class interest’ frame comes from a perspective. But it well describes circumstances where the wealthy get to determine policies that benefit themselves.

The New York Times recently ran two related stories that illustrate the issues raised here. The first is a series on the absentee owners of super-luxury real estate in Manhattan. It seems that real estate is exempted from anti-money laundering regulations so luxury real estate is both bank account and place to escape to for global kleptocrats when social accountability becomes an issue. The other is that contrary to recent efforts to give Wall Street cover for its crimes in the housing boom – bust, mortgage fraud by lenders really did lead to the housing bubble and subsequent bust and Great Recession. Neither of these are ‘accidents.’ They are the result of public policies that serve specific class interests.

Left unsaid, or rather carefully circumscribed to support siloed discourse, is that the political economy of the West is not working in political, economic, social and environmental dimensions. If ‘good’ public policies are possible without wholesale revolution, where are they? The rise of Syriza in Greece and Podemos in Spain are hopeful signs, but they are peripheral. Austerity forces in the Democrat-Republican coalition in the U.S. and the Troika in Europe conspicuously don’t care if the policies ‘work’ in the sense of being socially beneficial. And the refusal to address the broader pathologies of capitalism points to the hold that class interests have on public policies. With wars in Ukraine and Iraq looming, it is the Western ‘center’ that is the lunatic fringe.

Rob Urie is an artist and political economist. His book Zen Economics is written and awaiting publication. A sampling of Rob’s art can be found here.