“If it weren’t for the activity of investors, including large hedge funds, there would be no market recovery.”

— Larry Roberts, O.C. Housing News

There’s no doubt that housing prices are going up. According to Corelogic, home prices have risen nearly 10 percent in the last year. And sales have been improving, too. In fact, in the last year alone, sales for new “single-family” homes are up 28.9 percent (437,000 homes) while sales for existing homes have increased by 9.1 percent year-over-year. (4.92 million units)

At the same time, inventory is at a 13-year low, which is pushing prices even higher. Across the country, inventory is down 25.3 percent, but it’s much worse in some of the nation’s hotter markets. According to CNBC:

“Listings are down 31 percent in Seattle from a year ago, down 32 percent in Denver, down 20 percent in Houston, down 37 percent in Boston, according to local Realtor associations….

“At the moment it’s a seller’s market again,” said David Fogg, a real estate agent in Burbank, CA. “Very low inventory, very low interest rates, almost no bank inventory of homes, it’s crazy out there. Every good property I’ve listed this year has brought 10-50 offers and sales prices 10-20 percent over comps. Cash is King.” (CNBC)

So, if sales and prices are going up, and inventory is shrinking, then how can anyone dispute that housing is finally recovering?

While it’s true that the data don’t lie, it’s also true that there’s more in the data than meets the eye. For example, did you know that there are currently 9.8 million vacant housing units in the US, but only 1.74 million of those homes are listed for sale on the MLS? That’s less than 20 percent of the total. So where did the rest of the homes go? Did they just vanish into the ether or are they being kept off the market for some other reason, like to keep prices artificially high?

And as we said earlier, inventories are down 25.3 percent from 2012. There are two reasons for this. First, the banks are holding most of their distressed properties off the market to keep prices high. Second, the banks are controlling the number of underwater homeowners who are allowed to sell via short sales, that is, to sell their home for less than the current price of the mortgage. In other words, the banks control the whole shooting match. If the banks want prices to go up, they simply reduce the supply and prices edge higher. So far, the plan appears to be working.

Housing experts figure that roughly 40 percent of the people who would normally put their houses up for sale, are unable to do so because they are still underwater on their mortgage and the amount they’d get from the sale would require them to borrow money to pay the balance. Who wants to do that? It’s cheaper to just stay in the house and stop making the mortgage payment, which is what millions of people have done. Now they’re waiting for the bank to foreclose, but the banks are in no hurry because foreclosing would just add to their mountain of distressed inventory which would push prices down further. So millions of delinquent borrowers are presently living in their homes for free as they have been for the last two or three years. The “housing recovery” cheerleaders rarely mention this part of the story.

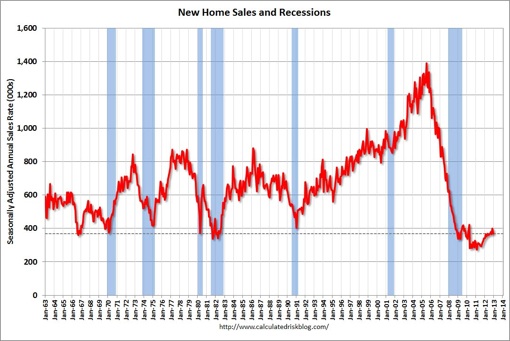

And another thing; while it may sound like houses are selling like hotcakes, the truth is far different. New home sales are less than one-third of what they were at their peak (1.4 million), while existing home sales are merely back to what they were in January 2002 before housing ballooned into a humongous bubble. In other words, the Fed’s record low rates, Obama’s mortgage modification programs, and FHA’s meager 3.5% down payment policy, have barely pushed sales back up to their historic trend. Does that sound like a strong recovery to you?

When you read about the great housing recovery, you should take it with a grain of salt. Take a look at this chart and you’ll see why.

See that little squiggle at the end of the red line? That’s the housing recovery. That’s what $1.5 trillion dollars worth of mortgage backed securities (MBS) will buy you these days. Such a deal!

Now check out this excerpt from The Burning Platform:

“The contrived elevation of home sales and home prices has been engineered by the very same culprits who crashed our financial system in the first place. This has been planned, coordinated and implemented by a conspiracy of the ruling oligarchy – the Federal Reserve, Wall Street, U.S. Treasury, NAR, and the corporate media conglomerates. Ben’s job was to screw senior citizens and drive interest rates low enough that everyone in the country could refinance, attract investors and flippers into the market, and propel home prices higher. Wall Street has been the linchpin to the whole sordid plan. They were tasked with drastically limiting the foreclosure pipeline, therefore creating a fake shortage of inventory. Next, JP Morgan, Blackrock, Citi, Bank of America, and dozens of other private equity firms have partnered with Fannie Mae and Freddie Mac, using free money provided by Ben Bernanke, to create investment funds to buy up millions of distressed properties and convert them into rental properties, further reducing the inventory of homes for sale and driving prices higher. Only the connected crony capitalists on Wall Street are getting a piece of this action. The Wall Street big hanging dicks have screwed the American middle class coming and going. The NAR and media are tasked with what they do best – spew propaganda, misinform, lie, cheerlead and attempt to create a buying frenzy among the willfully ignorant masses. ….. Mortgage applications by real people who want to live in a home are no higher than they were in 2010 when home sales were 33% lower than today. Mortgage applications are lower than they were in 1997 when 4 million existing homes were sold versus the 5 million pace today. The housing recovery is just another Wall Street scam designed to bilk the American middle class of what remains of their net worth.” (“It’s always the best time to buy”, The Burning Platform)

The whole article is a must read for anyone who’s at all interested in housing or government-Wall Street collusion. The author points to another disturbing trend too, the fact that firsttime homebuyers have vanished from the marketplace. Firsttime homebuyers and “move up” buyers used to make up the majority of all housing sales. Now they’ve been replaced by over-extended FHA borrowers (leveraged at 30 to 1) and private equity speculators who represent a full 30% of the market. This new dynamic won’t last, mainly because rising prices reduce profit margins causing speculators to shift to other forms of investment.

Case in point: Just look at Las Vegas where the big Wall Street investors have been buying everyhing that’s not nailed to the floor. This is from Realty Check:

“The Las Vegas market is being fueled by investors, but even the investors can’t find the great bargains anymore….(Mike Brunson, a local appraiser) called Las Vegas the Titanic of the real estate market. It was once thought unsinkable, and even now that the worst is over, he still thinks the market is on a well-provisioned life raft, not on solid ground.

“The only thing that concerns me is that we have been here before and the market itself is not what is driving the price increases. It’s not that we have new employers coming in and creating tens of thousands of new jobs that are leading to people buying new houses. It’s ‘Las Vegas is on sale,’ and investors are buying up everything they can in the used market…..

Brunson… still worries about the fundamentals, such as the slow economic growth and the fact that so much of the funding for new home sales is coming from low down payment, government-backed mortgages.” (“What’s Fueling the Housing Boom in Vegas?” Realty Check)

Brunson crystalizes the views of the housing skeptics (like me), that is, that a recovery that depends on speculators “chasing yield” instead of “organic growth” from working people looking for a place to live, is bound to fail. It’s only a matter of time. Any tightening of rates by the Fed or stock market correction will send the speculators racing for the exits.

Here’s more from Dave Dayen at The New Republic:

Analysts insist that REO-to-rental does not represent a bubble, that the rental revenue streams will satisfy investors and prevent a mass sell-off. But any disruption in the economy would affect the market for rental housing, leading to longer vacancies and lower returns on investment. And the textbook definition of a bubble consists of speculation chasing an appreciating asset. This is precisely what we have in REO-to-rental. In the words of analyst Josh Rosner of Graham Fisher, “the speculative boom has returned.”Investors have begun to pull out of one of the leading edge markets, Phoenix, as most of the foreclosed properties worth purchasing have been snapped up. The big run-up in prices there could collapse as demand collapses, depressing prices and putting the recovery in jeopardy. And any economic downturn would increase rental vacancies and send this entire market reeling. We may not only have a bubble, but already the beginnings of a bust….” (“Your new landlord lives on Wall Street“, Dave Dayen, The New Republic)

Once the PE parasites have stripped the carcas to the bone; they’ll move on to other prey. It’s the nature of the beast. That means that all the markets that rallied in the last 9 months, will see a sharp drop off in demand in 2013 as investment dries up and prices flatten out or retreat. The investment craze is on a very fixed time-line. If lending standards don’t ease, prices will fall. It’s a sure-thing. Low interest rates alone will not keep prices high.

Even so, Fed chairman Ben Bernanke’s zero rate policy (zirp) has helped to fuel another destructive bubble that is setting up borrowers for more excruciating losses. Take a look at the bubble that is developing in California. This is from an article titled More Bubble Trouble in California?:

“In Southern California, home sales have jumped 14 percent over last year and the median price is up 16 percent, some 25 percent in Orange County. We may not quite be at 2007 super-bubble levels but we’re getting there, particularly in the more desirable areas.

Yet, before opening the champagne, we need to look at some of the downsides of this asset recovery. We are not seeing much new construction, particularly of single-family homes, so the supply is not being replenished as inventory sinks. Meanwhile, many of the homebuyers are not families seeking residences, but flippers, Wall Street types and foreign investors. A remarkable one-in-three Southern California home purchasers paid with cash, up from 27 percent from last year.

It’s clear that this increase is not being fueled primarily by income growth among middle-class Californians; these “prices are rising disconnected from household incomes,” notes one analyst….

This leads to what is becoming the biggest problem facing the state – a decline in the rates of affordability. The previous bubble left us a legacy of more-affordable housing, an advantage we may now be losing….The groups hit hardest by this scenario will be middle- and working-class Californians, particularly above the age of 30-35, most of whom desire to own their own home. Unable to qualify, or unwilling to overleverage, many will be forced either to give up their dreams or look elsewhere, taking their talents and, eventually, their offspring, with them.” (“More Bubble Trouble in California?”, Joel Kotkin, New Geography)

As always, the Fed’s meddling creates clear winners and clear losers. In this case, working people are getting shafted while Ben’s facebook friends make off with the lion’s share of the loot. Some things never change.

There’s no way to dispute that prices and sales have been improving. Interest rate stimulus, inventory suppression, and unprecedented speculation have reversed the downward trend and lifted housing off the canvas. But it’s going to take more than that to produce a sustainable housing recovery. It’s going to take a strong economy where unemployment is low and wages are growing.

Don’t hold your breath.

Total Housing Activity Chart: http://advisorperspectives.com/dshort/charts/index.html?guest/2012/LR-Home-TotalActivityIndex-112812.PNG

MIKE WHITNEY lives in Washington state. He is a contributor to Hopeless: Barack Obama and the Politics of Illusion (AK Press). Hopeless is also available in a Kindle edition. He can be reached at fergiewhitney@msn.com.

{kind=link}